Unsecured home improvement loan options allow borrowers to access funds with no asset or other collateral attached as security. These options are mainly issued based on the borrower’s creditworthiness. You can get them as either personal loans or credit card loans.

High credit scores and excellent credit history, including higher income, are top requirements for this loan type. Based on these qualifying factors, it is not available to every applicant, with some lenders complicating the qualification criteria. Still, considering other available loan types from leading experts is vital.

Key Considerations Before Taking an Unsecured Home Improvement Loan

With an unsecured home improvement loan, your lender cannot foreclose your home if you default. While this sounds like an excellent solution to fund your renovation or remodeling project, there are still considerations to this loan type.

Shorter Repayment Terms

Before rushing to take this loan, it’s vital to understand that it comes with a shorter repayment term compared to other home improvement loan alternatives. A longer repayment period favors many borrowers because the monthly payments are usually lower, which allows for better budgeting. Shorter loan terms equate to high monthly installments.

Lower Loan Amounts

Because of the risk involved on the lender’s part, unsecured home improvement loans often come with lower loan amounts than other alternatives. Many lenders may allow you to borrow only up to $50,000, with a few extending the cap to $100,000.

Such amounts may not be adequate for funding your dream renovation. The amount approved against your creditworthiness may be lower than what an alternative home equity loan product would give you.

Higher Interest Rates Without Collateral

Unsecured home improvement loans are riskier for the lender, which may make them attract higher interest rates. The potentially high interest rate offsets the risk the lender assumes since it only depends on your creditworthiness. Still, you may save on high interest rates if you have higher credit scores.

Requires a Good Credit Score

Unlike other home improvement loan alternatives RenoFi presents, such as home equity loans or lines of credit (HELOC), other qualifying criteria for unsecured loans only depend on your creditworthiness. This means you will need a good and high credit score of at least 670 or above to qualify for higher loan amounts. Higher credit scores give you competitive loan terms and amounts.

Quick to Obtain

Since unsecured home improvement loans are based on your creditworthiness, they are quick to obtain if you have a good credit score. This quick funding means you can start your dream renovation without delay. Also, some lenders may not charge any fees for unsecured loans. Generally, these loan types feature quick funding with minimal charges compared to home equity loan products.

Types of Unsecured Home Improvement Loans

Unsecured loans are good options for borrowers with excellent credit scores. However, it’s vital to understand the available types of unsecured loans mainly:

Personal Loans

In most cases, home improvement loans include unsecured personal loans. However, it’s essential to understand such financing options and what you qualify to get. Generally, a personal loan is used for home renovations or remodeling and doesn’t require the borrower to put up their home or other assets as collateral. It’s also a reliable option for homeowners with minimal home equity.

Credit Cards

This is another form of unsecured loan used for home improvement. Credit card loans are recommended for minor home renovations since they attract higher interest rates than personal loans. The typically higher interest rates on credit cards make the overall renovation cost expensive. Using a card with a 0% introductory rate is also recommended to avoid paying interest.

Alternatives to Unsecured Home Improvement Loans at RenoFi

RenoFi understands various home remodeling funding models present several options for unsecured loans and may offer better alternatives for your home renovation project. This home renovation loan type combines the best features of a home equity loan and a construction loan, allowing you to borrow more money at the least possible cost.

It allows you to apply for a loan against your home after remodeling or renovation value, which taps into the remaining equity after the project’s completion without refinancing your first mortgage. It’s also excellent for new homeowners with minimal equity to qualify for other alternatives. RenoFi Loans:

- Have low fixed rates like traditional home equity loans

- Allows borrowers to get as much as 150% or 90% LTV

- Have the total loan amount available at closing

- Offer amounts from $20,000 to $500,000

- Up to 20-year term

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, let’s imagine that where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

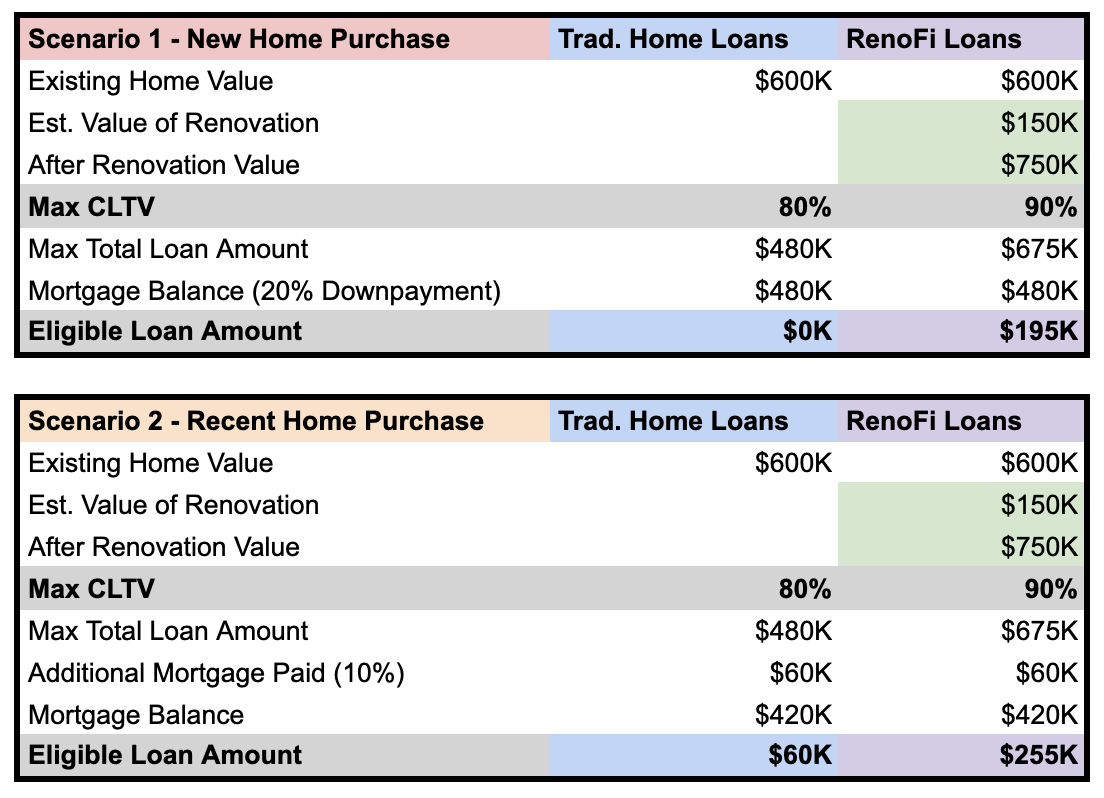

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Other alternatives include:

- HELOC: This loan allows you to borrow the money needed for home renovations up to a set limit, depending on your home equity. It uses your home as collateral, so failure to repay it may lead to foreclosure.

- Fixed Rate Home Equity: These loan types come with fixed interest rates without the need to refinance your first mortgage. The fixed-rate makes your monthly installments predictable and easy to budget.

- FHA 203k or Fannie Mae HomeStyle Loans: This government-backed home improvement loan alternative combines or bundles your mortgage and home renovation costs into one loan. It’s recommended for homeowners with less-than-perfect credit scores.

- Construction Loans: These loans allow you to borrow based on your home’s after-renovation value. However, you will have to refinance your existing mortgage and face higher closing costs than other alternatives. Construction loans also come with complicated processes that lead to project delays.

When You Should Consider Unsecured Home Improvement Loans

Generally, they are not top options for homeowners who have built equity. They are alternatives to finance your remodeling project if the entire cost is less than $20,000 to avoid attracting higher interest rates. It’s also suitable when you need fast funding for your project and have not built enough equity.

While this option is available for borrowers with good credit scores, talk to RenoFi to learn about other funding options for your larger and costlier dream home renovation projects that will require more funds. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80-85% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.