Residential construction loans are specialized financial tools designed to fund the construction or renovation of your primary residence. Unlike conventional loans, these are short-term loans that function as a line of credit, which provides the money as a one-time payment. Acquiring a residential loan is a complicated process that requires the borrower to research and plan.

In this guide, we will explain the requirements of a residential construction loan, its different types, and every other detail you need to know to finance the construction of your dream house smartly.

If you are looking for help with a construction loan, RenoFi offers construction loans through lending partners to help you find lenders for your property.

What Are Residential Construction Loans?

Residential construction loans are designed to cover the costs of constructing a new house. They are ideal financing options for property owners interested in building a custom-design property.

Construction loans are short-term, lasting approximately 12 to 18 months. They fund the expenses of buying the land or material, getting building permits, hiring contractors or labor, and putting aside money for contingency plans.

Rather than paying a lump sum of money like traditional mortgages, residential loans are disbursed during different stages of the construction. The borrower only needs to pay the interest during the building process.

Once the residence is built, the construction loan may be converted to a standard mortgage, requiring the owner to start repaying the borrowed money.

Residential Construction Loans vs Traditional Mortgages - What’s the Difference

While both are used to work on residential properties, construction loans and traditional mortgages differ significantly. They vary in terms of:

Purpose

Construction loans are used exclusively for building or renovating a home from scratch, while traditional mortgages are more concerned with the purchasing process for already-constructed properties.

Rates

Apart from the difference in their payment structure, construction loans tend to have significantly higher interest rates than traditional mortgages because, unlike conventional loans, there is no existing structure to serve as collateral. If the borrower defaults, the lender has little to gain from an unfinished property.

Down Payment

Construction loans usually require much stricter and higher down payment requirements to lower the risk of defaulting. These financing options require a down payment of about 20% of the loan amount, compared to the 3 to 5% required by standard mortgage loans.

How Do Residential Construction Loans Work?

Construction loans work slightly differently than regular home loans. The first step is to apply for the loan alongside details of the project design, construction timeline, and estimated budget.

Once the lender has reviewed and approved the application, the interest rate, repayment period, and other loan terms are decided. During the property’s construction, the lender directly provides the amount in installments (draws) to the builder instead of the borrower.

Each draw is linked to completing a single phase, such as laying down the structure or framing the house. The lender may also send an inspector to inspect the finishing of each stage before sending in the next draw.

An essential factor is that most residential loans have variable interest rates, which may increase or decrease depending on market value. Once the project is completed, the construction loan is either converted into a permanent mortgage or requires you to qualify for a new mortgage to repay the borrowed amount.

Types of Residential Construction Loans

While all residential loans help finance the property’s buildup, they have distinct features that make them suitable for unique situations. Here’s an overview of the three most common types of construction loans:

Construction-Only Loan

Interim or construction-only loans are high-risk finance options that must be paid off as soon as the project is completed. They are also known as ’two-close’ loans. This type is ideal for borrowers who plan to repay the loans by selling their old property.

Construction-to-Permanent Loan

As their name suggests, construction-to-permanent loans simplify the repayment process by combining the construction and permanent mortgage into a single loan. These short-term loans automatically close upon project completion and convert into a fixed- or variable-rate traditional mortgage. This type suits property owners looking to save up on closing costs.

Renovation Construction Loan

Renovation construction loans, insured by the Federal Housing Administration (FHA), cover the expenses of purchasing and renovating a property. They are also known as 203(k) loans and are perfect for investing in fixer-uppers and other structures needing extensive remodels.

Construction loans are primarily used for new construction or major remodeling projects, while RenoFi loans are designed for major home renovations.

For many homeowners, a traditional home equity loan is something many use to do large renovation projects. Let’s imagine a scenario where you want to get a home equity loan instead of a construction loan to get $150,000 to renovate your new home and increase the value of your home by $150,000:

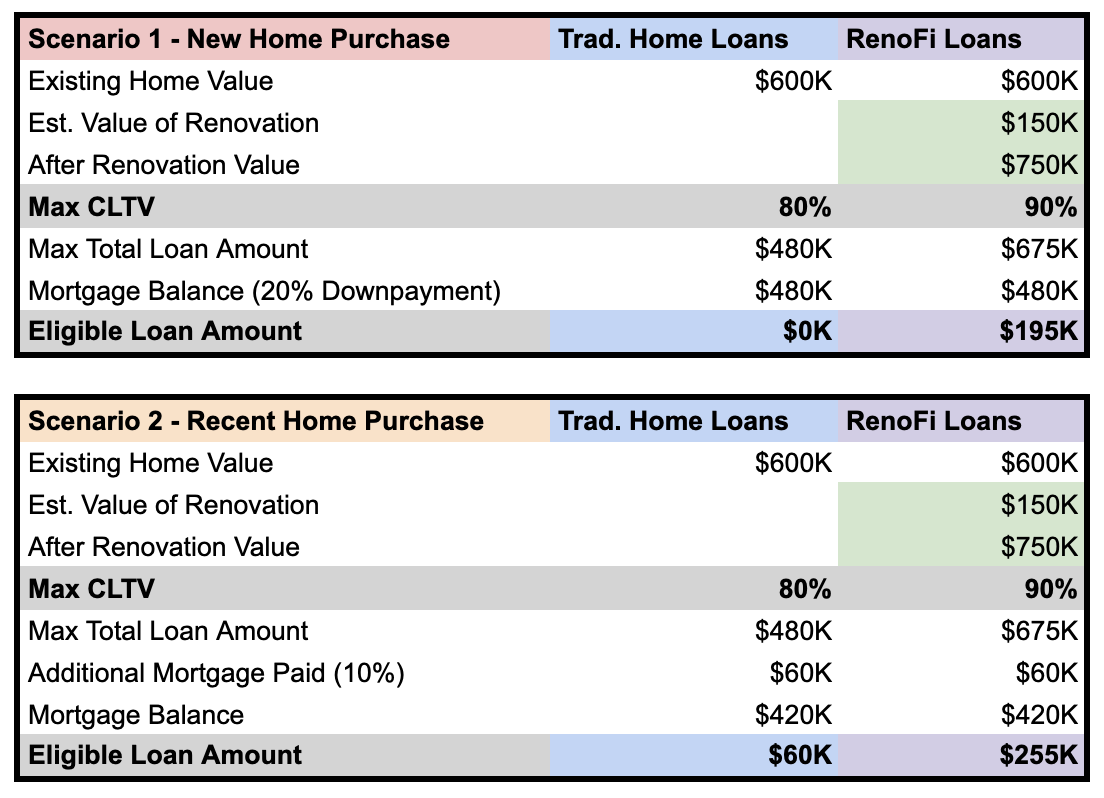

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereResidential Construction Loan Requirements

You must have your ducks in a row to easily qualify for the residential construction loan. This includes:

- Maintaining a good credit score: An excellent credit score, between 680 and 720 or higher, increases your chances of attracting a lender and helps you secure a construction loan quickly.

- Having a stable income: It is essential to verify your income documentation and have a low debt-to-income ratio (possibly 35% or less) to pay off the loan while fulfilling other financial duties.

- Working with an experienced contractor: Most construction loans require the borrower to contact a qualified and licensed contractor who can oversee the project’s progress.

- Providing project details: The clearer your architectural plans, the higher the chances of the lender approving your request. Prepare designs, estimated budgets, and project timelines under an expert’s supervision.

Conclusion

Navigating the intricacies of a residential construction loan alone can be challenging. At RenoFi, we are committed to helping you find the funding you need. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.