Renovation loan requirements are key to understand when planning a home improvement project, especially when you are considering options that offer more flexibility, like RenoFi loans. If you’re new to home improvement financing, these requirements can be complicated. Many homeowners may be familiar with traditional options like home equity loans or cash-out refinances, but these aren’t always the best fit for everyone’s renovation needs.

This is where RenoFi Loans come into play. Unlike traditional renovation loans, RenoFi loans offer a unique approach by leveraging the after-renovation value of your home. This means you can access more funds without refinancing your existing mortgage or dealing with the hassles of traditional loan requirements.

Whether you’re thinking of adding an extra room, upgrading your kitchen, or completely transforming your home, knowing the ins and outs of what lenders look for can help streamline the process. This article will cover the essential requirements for renovation loans, including credit score expectations, income requirements, and other factors influencing loan approval.

What Is a Renovation Loan?

A renovation loan is a type of financing that helps homeowners fund major home improvements by using their property as collateral.

Unlike traditional loans, renovation loans work a bit differently. Instead of just looking at your home’s current value, they consider what it’s worth after you make those changes, which can unlock more borrowing power. This is helpful if you don’t have a lot of equity in your home or don’t want to refinance your current mortgage.

For instance, RenoFi loans work by factoring in the home’s after-renovation value (ARV), enabling homeowners to borrow more than traditional loans would allow.

General Renovation Loan Requirements

To get a renovation loan, you’ll need to meet certain requirements. Here are the main things lenders will consider:

Credit Score

Your credit score plays a significant role in qualifying for a renovation loan. Generally, lenders require a minimum credit score of 620 for renovation loans. However, a higher credit score, typically 680 or above, may provide better terms, such as lower interest rates and higher loan amounts.

RenoFi loans also consider your credit score but may offer more favorable terms for homeowners than traditional loans.

Debt-to-Income Ratio (DTI)

Your DTI ratio measures your debt compared to your income. It gives lenders an idea of how much money you have in your budget to handle additional loan payments.

Most lenders look for a DTI ratio below a certain threshold, typically around 36% or lower. This means that your total monthly debt payments shouldn’t exceed 36% of your gross monthly income.

RenoFi loans generally follow this guideline but may allow more flexibility, especially if the renovations significantly increase your home’s value.

Equity in Your Home

Equity is one of the primary considerations when securing a renovation loan. Your home equity is the money you’d get if you sold your house and paid off the mortgage.

To calculate your home equity, take the market value of your home and subtract the remaining balance of your mortgage. For traditional home equity loans or lines of credit (HELOCs), you typically need at least 20% equity to qualify.

However, RenoFi loans are unique in that they allow homeowners to borrow based on the home’s future value after renovations. This means you can borrow more than what your current equity would allow, offering a much-needed alternative to traditional equity-based financing options.

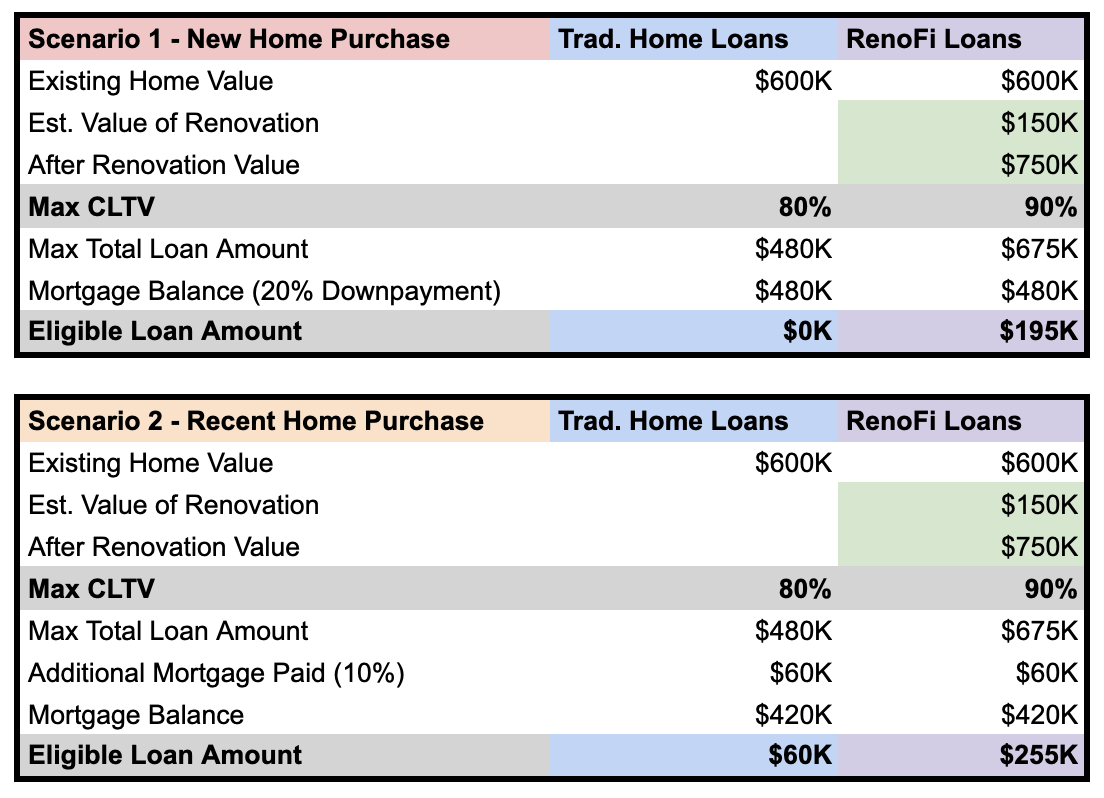

For example, let’s imagine you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Appraisal Requirements

Lenders often require an appraisal to determine the value of your home and its future value after renovations. For most renovation loans, an appraiser evaluates your home based on its current condition and renovation plans.

RenoFi takes this one step further by using the after-renovation value (ARV), often higher than a current market appraisal. This can greatly increase your borrowing power.

Loan-to-Value Ratio (LTV)

When you get a renovation loan, the lender will calculate a loan-to-value ratio. This is the amount you borrow compared to the value of your home.

Most lenders set a limit of 80% to 90%. However, RenoFi loans use the after-renovation value, allowing you to borrow up to 150% LTV, a significant advantage over traditional home equity loans.

Additional Requirements for Specific Loan Types

Different types of renovation loans have different requirements. Let’s examine the most common options and what they require from you.

FHA 203(k) Loans

FHA 203(k) loans are popular for homeowners with limited equity or those seeking to combine renovation costs with their primary mortgage. To get an FHA loan, you’ll need a credit score of at least 580. If you have a score of 580, you’ll need a down payment of 3.5%. But if your score is 500, you’ll need a down payment of 10%. However, the total loan amount cannot exceed the FHA loan limits for your area.

While FHA loans can be a great option, they often require draws and inspections. This means the lender will release funds in stages as work is completed. In contrast, RenoFi loans provide upfront financing, allowing you to manage your renovation more efficiently.

Fannie Mae HomeStyle Renovation Loans

The Fannie Mae HomeStyle loan is another option that combines a home purchase or refinance with renovation financing. These loans typically require a minimum credit score of 620 and allow borrowers to finance up to 75% of the home’s after-renovation value.

However, these loans often come with more stringent appraisal and inspection requirements, adding complexity to the process. RenoFi loans, by comparison, are generally more straightforward, with fewer inspections and more flexibility.

How RenoFi Loans Can Help

RenoFi loans offer a powerful alternative to traditional renovation financing. Instead of relying solely on your current home equity, a RenoFi loan allows you to borrow based on the after-renovation value of your home. This is particularly helpful for homeowners undertaking larger projects exceeding their home equity.

Additionally, RenoFi loans do not require you to refinance your existing mortgage, meaning you can keep your current low rate while still gaining access to the funds you need.

Get started with your RenoFi loan hereConclusion

Understanding renovation loan requirements is crucial for homeowners, especially if they are considering a significant renovation project. From credit scores and DTI ratios to appraisal requirements and loan types, several factors must be considered.

While traditional home equity loans and FHA 203(k) loans may offer viable options, RenoFi loans stand out as a flexible and powerful alternative. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.