Refinancing loans or using home equity loans are reliable tools for homeowners to access cash, lower monthly payments, or save cash on interest. Refinancing pays off or replaces your current or old mortgage in exchange for a new one with lower interest rates, while a home equity loan gives you access to funds against your home’s equity, usually at a competitive interest rate.

Choosing the best for your situation really depends on your repayment ability, credit score, and other eligibility criteria.

Eligibility for a Refinance or Home Equity Loan

When looking for a refinance, most lenders require homeowners to have at least a 580 credit score and about 620 for a cash-out. However, these may vary depending on the lender.

Meanwhile, to be eligible for a home equity loan, you must have a minimum of 20% equity in your home, with some lenders allowing 15%. You will also need a loan-to-value ratio (LTV) of at least 80%.

Refinance

While refinancing replaces your old mortgage with a new and larger one, you will pay a higher interest rate on cash-out refinance than rate-and-term refinance. A refinance is determined by the bank standards, your credit profile, and your home’s LTV. Your lender will also assess the term of your previous loan and the balance to be paid off. When choosing this option, it’s vital to consider the pros and cons.

Pros of a Refinance

- Interest is tax-deductible

- You can use the cash in any way

- You get a lower interest rate than the current mortgage

- It consolidates high-interest debts into one monthly payment

- It boosts your home’s value if you use the cash for improvements

Cons of Refinance

- It may sometimes attract higher interest rates or other costs

- Underwriting standards are higher

- It requires a low debt-to-income ratio

- Property value decline can lead to more than your house value

RenoFi Cash Out Refinance

A cash-out refinance replaces your current mortgage with a new mortgage that is greater than what you currently owe with a different interest rate and payment amount. Unlike Home Equity Loans, a Cash Out Refinance is a brand new loan with a different interest rate rather than a second loan on top of your existing loan.

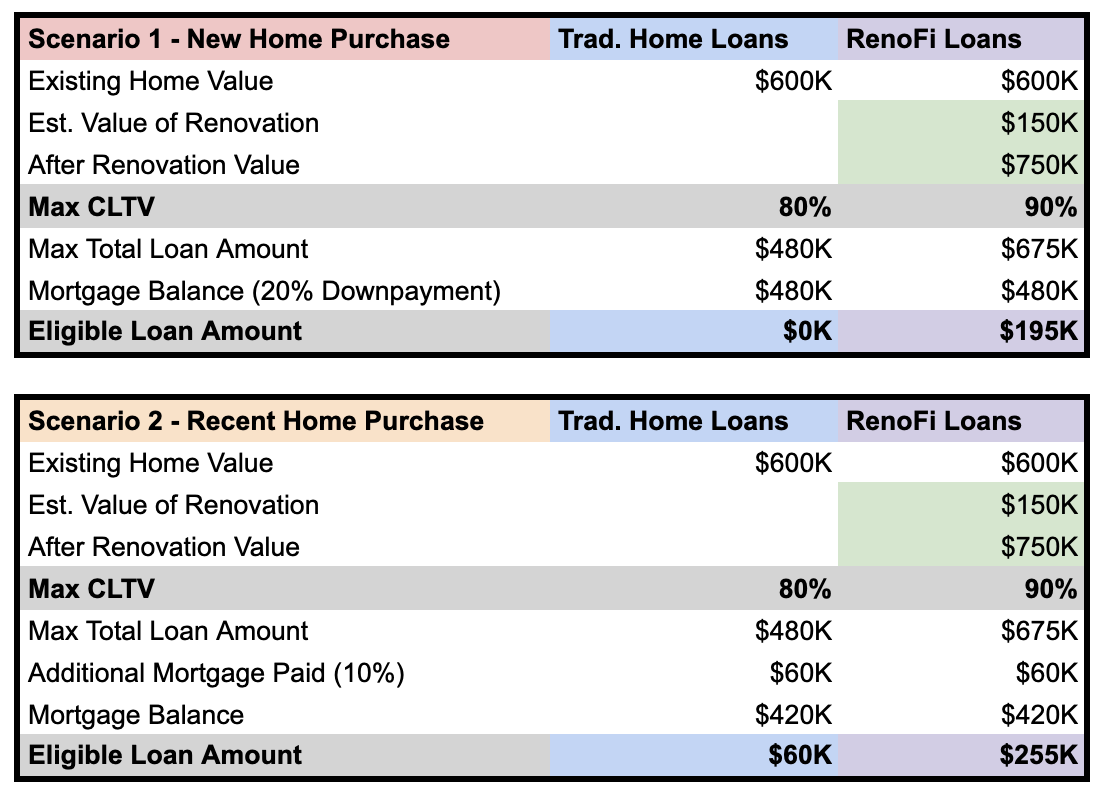

Let’s imagine a scenario where you want to borrow $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Home Equity Loan

Generally, like most home renovation and remodeling loan options, this type allows you to borrow against your home’s equity and usually has lower interest rates than personal, unsecured loans because your home is the collateral.

Pros of Home Equity Loan

- Excellent for significant projects like home improvements

- Gives you access to the cash value of your home without reselling

- The interest may be tax-deductible, reducing the overall tax burden

- Predictable monthly installments and fixed rates

Cons of Home Equity Loan

- If you default, you can lose your home

- You will need higher credit requirements than cash-out refinance

- You will have two loans to repay besides the existing mortgage

- The sum amount is fixed

RenoFi Home Equity Loan

Using the same example above where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereRefinance and Home Equity Loan Differences

Since both give you access to funds for your renovation, remodeling, or other home-related and lender-approved uses, choosing the right one for you may be challenging if you don’t understand how they differ. Here are some key differences.

- Refinance generally has lower interest rates than home equity loan

- Home equity loan has shorter repayment terms, while refinance have longer terms

- Home equity gives you a second mortgage, while refinance replaces your current mortgage with a new but larger one

Refinance and Home Equity Loan Similarities

While home equity loans and refinance aim to give homeowners access to funds, determining the right fit for your needs is vital. This is why it’s vital to consider their similarities to help you make the right decision. Some common similarities include:

- Both options utilize your home’s value as collateral or security for the loan

- Interest paid may be tax-deductible

- Lenders will require you to retain some equity in your home

Refinance vs Home Equity Loan: Choosing the Right Option

While both refinance and home equity loans have their pros and cons, to choose the right option, you should consider how each financing option benefits and suits your specific financial need. Here are some factors to help you decide the best move to take:

Clearly Define Your Primary Goal

If you are looking to get substantial cash to finance your home upgrade or remodel and, at the same time, lower your monthly mortgage payment through a low-interest loan, then refinancing might be ideal for you. On the other hand, if your primary goal is only to get funds for your new project, then consider a home equity loan.

Understand Your Credit Score

Your credibility to get either a refinancing or home equity loan depends on your credit score. If you have a low credit score, a home equity loan is the best option, and it can get you as much equity as a cash-out refinance. However, if your credit score is higher than when you originally bought your home, refinancing might be in your best interest.

Compare Closing Costs

A home equity loan has a lower closing cost than a refinance and is less complex to obtain. Cash-out refinance tends to be more expensive regarding fees because of higher underwriting standards. With RenoFi’s home equity loan, you can be assured of competitive interest rates and fees to help you get the value for your hard-earned money.

Other Factors

If you are unsatisfied with your current mortgage and want possibly new mortgage rates and favorable terms, then refinancing can be great. However, if your current mortgage is satisfactory, consider a home equity loan, as it is less expensive for homeowners who require access to cash.

Conclusion

Both refinance and home equity loan options provide a means of getting the value of your equity. Whether you prefer a home equity loan or refinance, it depends on your primary goal, financial profile and requirements. Additionally, our RenoFi loans are the smartest way to finance a home renovation project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.