Owner builder construction loans are for those who want to build their own home while acting as their own contractor. Like a traditional construction loan, this option lets you fund your new build but eliminates contractor markups and fees, which can help you save money if you manage the project well.

This guide will explain how these loans work, what qualifications you need, and some alternatives to consider.

What Is an Owner Builder Construction Loan?

An owner-builder construction loan lets you take control of your home construction. With this arrangement, you’re both the owner and the general contractor. This is different from a standard construction loan, where a licensed contractor handles the project.

By managing the home construction yourself, you could save on labor costs. However, this also means you’ll take on extra responsibilities, such as getting permits, coordinating subcontractors, and making sure the project stays on schedule.

Key Differences Between Owner-Builder and Construction Loans

Owner builder construction loans give you, the homeowner, full control over your construction project. This means you can choose subcontractors, materials, and design features that fit your vision. With this hands-on approach, you’ll avoid contractor fees and likely save money.

Like traditional construction loans, owner-builder loans provide funds in stages, usually based on project milestones. But the difference is that you manage these funds yourself. This lets you budget effectively and oversee everything throughout the building process to make sure your project stays on track.

In summary, owner-builder construction loans offer a more personalized and potentially cost-effective way to build a home.

How to Qualify for an Owner Builder Construction Loan

- Construction Experience: Lenders generally only lend to borrowers who are licensed contractors with past building experience. This background shows you understand the complexities of managing a building project. Without past experience building houses, you are very unlikely to receive a loan from a lender.

- Solid Construction Plan: You’ll need a clear construction plan that outlines your project’s scope, timeline, and budget.

- Credit Requirements: Lenders typically look for a credit score of at least 680 or higher, depending on their specific criteria. Since lenders see these loans as a bit riskier than traditional mortgages, they usually impose stricter standards, so you might face higher interest rates or more challenging approval processes.

- Down Payment: While the exact amount can vary based on the lender, type of construction loan, and financial situation, most lenders typically require around 20% to 25% (or even higher) of the total project cost as a down payment.

Steps to Getting an Owner Builder Construction Loan

- Find Your Property: First, look for suitable land for your new build. Consider the location, size, and any zoning restrictions that might affect your plans.

- Choose a Lender: Do some digging to find lenders that specialize in owner-builder loans. It’s worth checking reviews and comparing rates to find one that suits your needs.

- Prepare Documentation: Gather all the necessary paperwork, such as income verification, credit reports, and your detailed construction plan.

- Obtain Pre-Approval: Getting pre-approved will give you a clear idea of your budget and help you plan your project without any surprises.

- Finalize Loan Terms: Once you’ve found the right lender and got your pre-approval, close the loan agreement and get ready to start building.

Advantages of Owner Builder Construction Loans

Being an owner-builder offers some great benefits:

- Cost Savings: By acting as your own general contractor, you can skip contractor fees and markups, potentially saving a significant amount on your build.

- More Control: You get to choose subcontractors and materials. Plus, you can make decisions that match your vision. This allows for more customization.

- Budget Flexibility: With owner builder loans, you have more control over your budget, so you can allocate funds as needed and make adjustments throughout the project based on real-time expenses and progress.

- Personal Satisfaction: There’s a special sense of accomplishment in building your own home and seeing your ideas come to life.

Potential Downsides of Owner Builder Construction Loans

While owner builder construction loans can be attractive, they do come with many difficult challenges:

- Complicated Loan Process: The application can be trickier than standard loans, requiring more detailed paperwork and planning. In addition, banks will typically only lend to licensed contractors which means you will need to have all the licenses in place before you receive the money.

- Project Management Responsibility: You’re in charge of managing every part of the build, which can get overwhelming and eat up your time.

- Cost Overruns and Delays: Without a professional overseeing things, unexpected expenses and delays can pop up more easily.

- Draws: Funds are released in stages based on project milestones. If your construction slows down, you might run into cash flow issues while waiting for the next draw.

- Inspections: Each draw usually requires inspections to ensure the work meets standards. While this keeps everyone accountable, it can also slow you down if any issues arise.

RenoFi Loans: A Smart Alternative

RenoFi loans are great for homeowners looking to finance big renovations or home additions. They let you access your home’s equity without having to refinance your first mortgage. This makes it simpler to fund your upgrades while keeping your current low interest rate.

Why a RenoFi Loan Makes More Sense for Your Renovation Project

If you’re looking to improve your current home instead of starting fresh with a new build, an owner builder construction loan might not be the best fit. Before jumping into traditional financing options, keep in mind they usually limit how much you can borrow based on your current equity.

Take a traditional 90% LTV HELOC, for instance. It might seem like a solid choice for funding your home renovation, but it often doesn’t give you enough equity to cover everything on your wishlist. A smarter move is to consider the After Renovation Value of your home, which is what RenoFi loans use to boost your available equity.

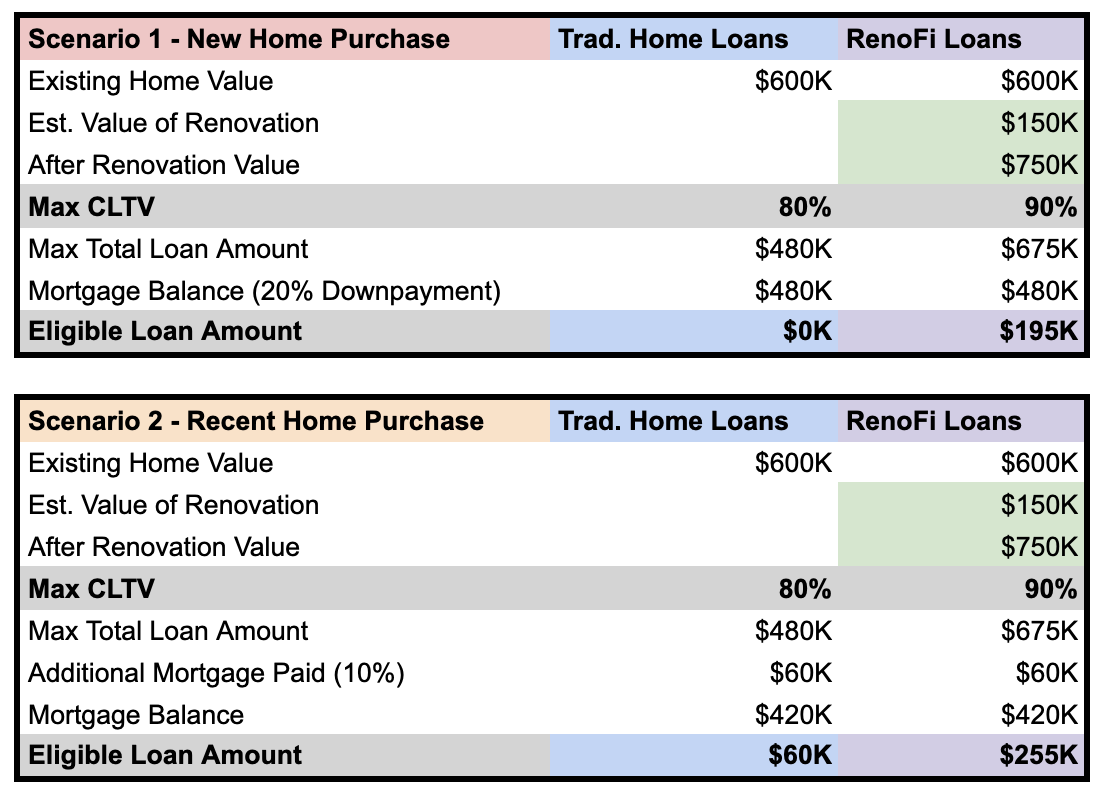

Let’s imagine a simple example where you are comparing a home equity loan with a RenoFi home equity loan and you want to borrow $150,000 for renovations that you believe will increase the value of your home by $150,000.

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your eligible loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereUpgrade Your Home the Smart Way With RenoFi

While owner-builder construction loans can be great for new home builds, RenoFi loans offer a simpler alternative for homeowners looking to renovate. If you’re considering renovations and want an efficient financing solution, RenoFi can help streamline the process. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.