A construction loan gives you the money you need to build your home. It’s usually short-term, lasting only for the time it takes to finish the build. Once your home is complete, the loan can either roll into a regular mortgage, or you might need to pay it off in full.

Construction loans typically require a full refinance and are based on the current value of your home. They also involve more complex draw schedules and inspections, which can add time and complexity to your project.

In contrast, RenoFi loans are tailored specifically for renovations. RenoFi loans don’t require refinancing your mortgage, have no draw schedules, and leverage your home’s future value to allow you to borrow up to 11x more money for renovations. This makes RenoFi loans a more convenient and cost-effective choice for homeowners who want to tackle large-scale renovations without the headaches that come with traditional construction loans.

If you are looking for help with a construction loan, Renofi offers construction loans through lending partners to help you find lenders for your property.

How to Get a Construction Loan

Step One: Start by Finding a Licensed Builder

Do some research and find a reputable builder with proven expertise. Check credentials and compare quotes to find one that best fits your budget and project. The NAHB directory of local home builders associations can help you find licensed contractors in your area.

Step Two: Find a Construction Loan Lender

Renofi offers construction loans through lending partners so that you can compare rates and terms to help you find lenders for your property.

Step Three: Gather Your Documents

Prepare a detailed contract with your builder, making sure to include pricing and project plans. Gather all of your personal documentation like pay stubs, tax returns, and proof of income that you would need for a traditional mortgage.

Step Four: Get Prequalified

Getting prequalified gives you an idea of how much you can borrow and helps ensure that your project plans align with your budget. If you don’t get enough money for your renovation project, consider applying for RenoFi loans which use the after-renovation value of your property and increase your borrowing power.

Step Five: Acquire Homeowner’s Insurance

As a final step, you may want to purchase a homeowner’s insurance policy with builder’s risk coverage to protect against any issues that may come up during the construction phase.

Types of Construction Loans

Construction-Only Loans

These loans only cover the construction costs. Once you finish building, you must pay off the loan in full, which means you’ll want to have a plan for financing afterward, whether through refinancing or taking out a different loan.

Construction-to-Permanent Loans

These loans start as construction financing but convert into a standard mortgage once the building is complete. It’s a simpler option because you won’t need to take out a separate mortgage later. Also, you’ll make monthly payments based on the total loan amount, making the transition smoother.

Owner-Builder Loans

If you plan to act as your own general contractor, an owner-builder loan could work for you. However, lenders usually have tougher requirements for owner-builders.

Land Loans

A land loan helps you buy land for building your dream home. This land can be improved, meaning it has some basic infrastructure, or is unimproved, which is raw land. Since these loans carry more risk, you’ll usually see higher interest rates and down payments.

Rehab Loans

This type of loan covers both the purchase of an existing home and any renovations you plan to make. The funds are released in stages as you hit project milestones, and during the renovation period, borrowers often only pay interest. These loans are typically short-term and convert to a traditional mortgage once the renovations are finished.

End Loans

An end loan is a mortgage that steps in once construction is done. It simplifies everything by merging your construction and permanent loan into one. With this loan, you’ll make regular principal and interest payments, making it easier to manage your finances.

What You Need to Qualify for a Construction Loan

To qualify for a construction loan, you’ll need to meet a few important requirements:

- Credit Score: Most lenders look for a credit score of at least 680. If your score is higher, you’ll have a better chance of getting approved, and you might qualify for better interest rates.

- Down Payment: You’ll likely need to put down 20% to 25% of the project’s total cost, but some lenders might offer different terms, so it’s worth shopping around.

- Detailed Plans: Be ready to show details of your construction plans and timelines. Lenders want to know exactly how you plan to build your home.

- Proof of Income: You’ll need to show your financial stability with bank statements, pay stubs, or tax returns. Lenders want to be sure you can repay the loan.

Things to Consider With Construction Loans

While construction loans can be a great option, here are a few things to keep in mind:

Interest Rates

These loans might have higher interest rates compared to traditional mortgages, but that depends on your credit score, the lender’s terms, and market conditions. This could increase your overall borrowing costs, so it’s usually a good idea to shop around for the best rates or consider alternative financing options like the FHA 203(k) loan.

Complex Process

Getting and managing your funds can be a bit complex. You’ll likely encounter draw schedules, where the lender releases funds in stages. Additionally, various points of the project require inspections before funds are released. These requirements add extra layers to the process and can be frustrating for you and your contractor.

Risk of Delays

If your project faces delays or cost overruns, it can create significant financial strain. Unexpected issues, such as material shortages or weather delays, can push costs higher and extend the timeline. This means you could end up making extra interest payments on your construction loan, which might affect your overall budget.

RenoFi Loans as an Alternative

If you’re looking to renovate rather than build, RenoFi loans offer a unique solution. These loans let you borrow against your home’s future value after renovations are complete. This means you don’t need extensive equity in your current home, making it easier to access funds for significant improvements.

Like many homeowners, you might be considering a traditional HELOC or home equity loan, especially if you’ve decided that a construction loan isn’t the best fit for your remodeling project.

While a traditional 90% LTV HELOC may seem like a good option for funding your home renovation, it often doesn’t provide enough equity to cover your entire wishlist. A better solution is to consider the After Renovation Value of your home, which RenoFi loans use to boost your available equity.

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

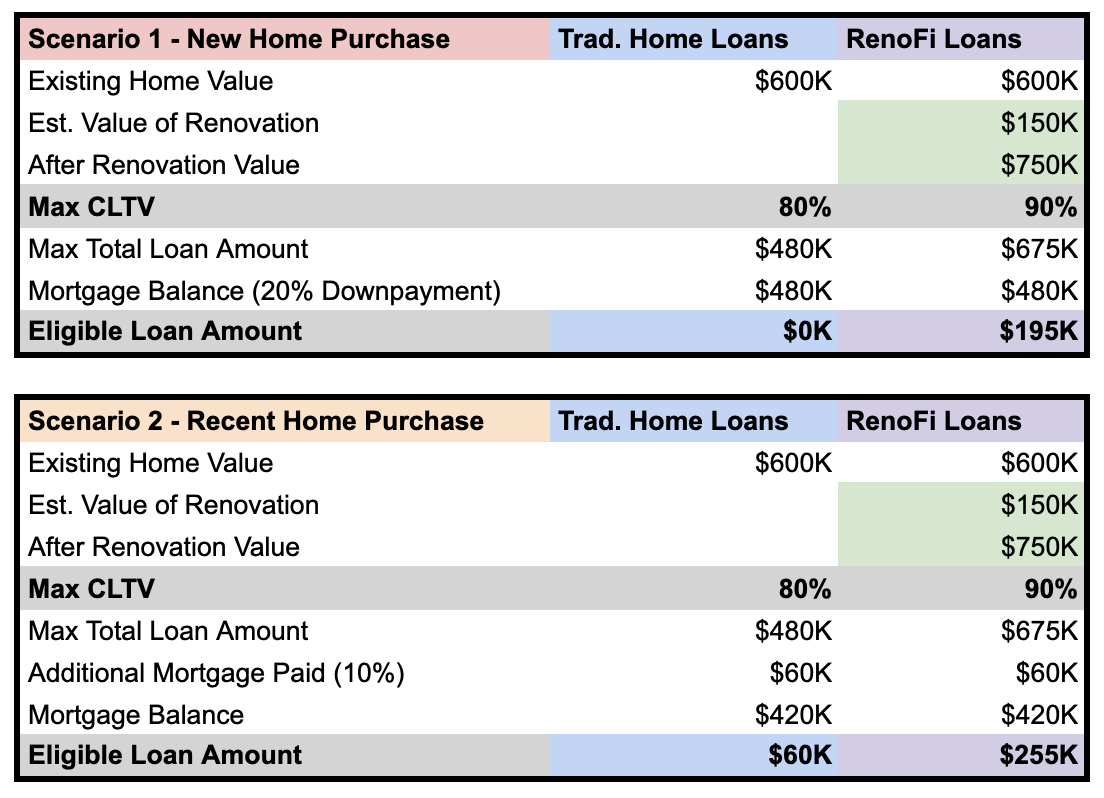

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s imagine you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereLet RenoFi Help With Your Home Renovation Project

Knowing how to get a construction loan for a house involves understanding its unique features and requirements. If you’re considering renovations instead of building from scratch, RenoFi can help you access funds based on your home’s future value.

Additionally, our RenoFi loans are the smartest way to finance a home renovation project. Unlike traditional loans, which are based on your current home value or require you to refinance your primary mortgage and give up your low rate, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Contact us today to learn more about how we can help you obtain the funds you need for your major renovation project.