To get a construction loan, prepare the project costs, select a credible builder, and apply with a lender who releases money in stages during construction. Construction loans are short-term loans designed to help you pay for building new structures, like a house or an ADU. They’re primarily meant to create something new from the ground up, but you can also use them for major renovations.

Since construction can be a bit unpredictable, these loans usually have a higher interest rate than traditional mortgages and require a clear plan and budget.

If you are looking for help with a construction loan, the Renofi Marketplace offers construction loans through lending partners to help you find lenders for your property.

How Construction Loans Work

Construction loans are a bit different from regular mortgages. When you apply for one, lenders want to see a detailed plan that shows how much your project will cost and how long it will take. This helps them figure out how much money you need and when you’ll need it.

Instead of giving you the full loan amount all at once, the money is released in stages, called “draws,” as your construction progresses. For instance, you might get some money upfront for site preparation and laying the foundation and then more funds as you hit different milestones in the building process.c

During the construction phase, you usually only pay interest on the amount you’ve drawn so far. This keeps your costs lower while you’re building. Once everything is finished, the loan can either turn into a traditional mortgage or be paid off with another loan, depending on what you and your lender agreed upon.

Types of Construction Loans

- Construction-to-Permanent Loans: These start as short-term loans for construction and automatically convert to a permanent mortgage once the project is completed.

- Stand-Alone Construction Loans: These are short-term loans used only during construction. After the project, you’ll need a separate mortgage to pay it off.

- Renovation Loans: Ideal for remodeling or adding to an existing home, these loans consider the future value of your home after improvements.

- Owner Builder Loans: If you plan to act as your own general contractor, these loans let you manage the construction process directly. Lenders send the funds directly to you, not to a contractor, but they usually ask for proof that you have experience or a contractor’s license.

- Bridge Loans: These short-term loans are designed to cover costs while you secure a permanent loan. They’re especially helpful if you’re building a new home and selling your current one at the same time, so it’s easier to cover the gap in financing.

- End Loans: Once construction is done, an end loan pays off your short-term construction loan. It gives you long-term financing with stable monthly payments moving forward.

How to Get a Construction Loan for Your ADU Project

- Choose a Licensed Builder: Lenders want to see that your builder has the skills to complete the job. Ask for recommendations from friends or check local builder directories to find qualified contractors.

- Find a Lender: Look for lenders who specialize in construction loans. Compare their rates, terms, and down payment requirements to find the best fit for your needs.

- Gather Your Documents: Prepare a contract with your builder that outlines project costs and plans. You’ll also need financial documents, like pay stubs and tax returns, to prove your income and assets.

- Get Preapproved: Getting preapproved will help you understand how much you can borrow so you don’t waste time on plans that exceed your budget.

- Secure Homeowners Insurance: Your lender will likely require a homeowners insurance policy with the builder’s risk coverage. This protects against any issues during construction.

What to Keep in Mind When Financing Your ADU Project

Taking out construction loans for home additions might seem like a good idea since many homeowners see them as short-term builder loans. But this might not necessarily be the right financing option, especially if you don’t have a lot of money to start with. Here are some key things to keep in mind:

Short Repayment Periods

If you’re looking to get a construction loan, it’s super important to keep an eye on your construction timeline. Here’s why.

Banks usually give you about 12 to 18 months to complete the project. However, getting permits can take up to 6 to 8 months or more. If you don’t have enough funds at the beginning, you might want to look into home equity loans or lines of credit instead.

Complex Draw Process

Construction loans work by giving you the money in installments or draws. This means you or your contractor will receive funds at different stages of the project. If your project needs a lot of upfront costs that exceed the first draw, it could affect your cash flow.

Conversion and Refinancing Can Change Interest Rates

Remember that construction loans are short-term. Once your project is done, they usually convert into permanent mortgages, which means you might need to refinance. This means you may have to give up any existing favorable interest rates you’ve locked in.

Higher Costs Ahead

Be ready for higher interest rates and fees compared to traditional mortgages. These extra costs can add up and make your project less appealing financially in the long run.

If you are looking for help with a construction loan, the Renofi Marketplace offers construction loans through lending partners to help you find lenders for your property.

Why a RenoFi Loan Is Best for ADUs or Home Additions

Instead of using construction loans, RenoFi is a smarter choice for financing an ADU project. Adding an ADU can significantly increase the value of your property and create future cash flows if you decide to rent it out.

That said, building an ADU is quite expensive and often requires financing. Even if you opt for a traditional home equity loan rather than a construction loan, you’ll need a significant amount of equity in your home.

That’s where RenoFi comes in as a perfect solution. RenoFi leverages the after-renovation value of your property, which means it uses the increased value of your home once the addition or ADU is complete. This boosts your available equity and increases your borrowing power.

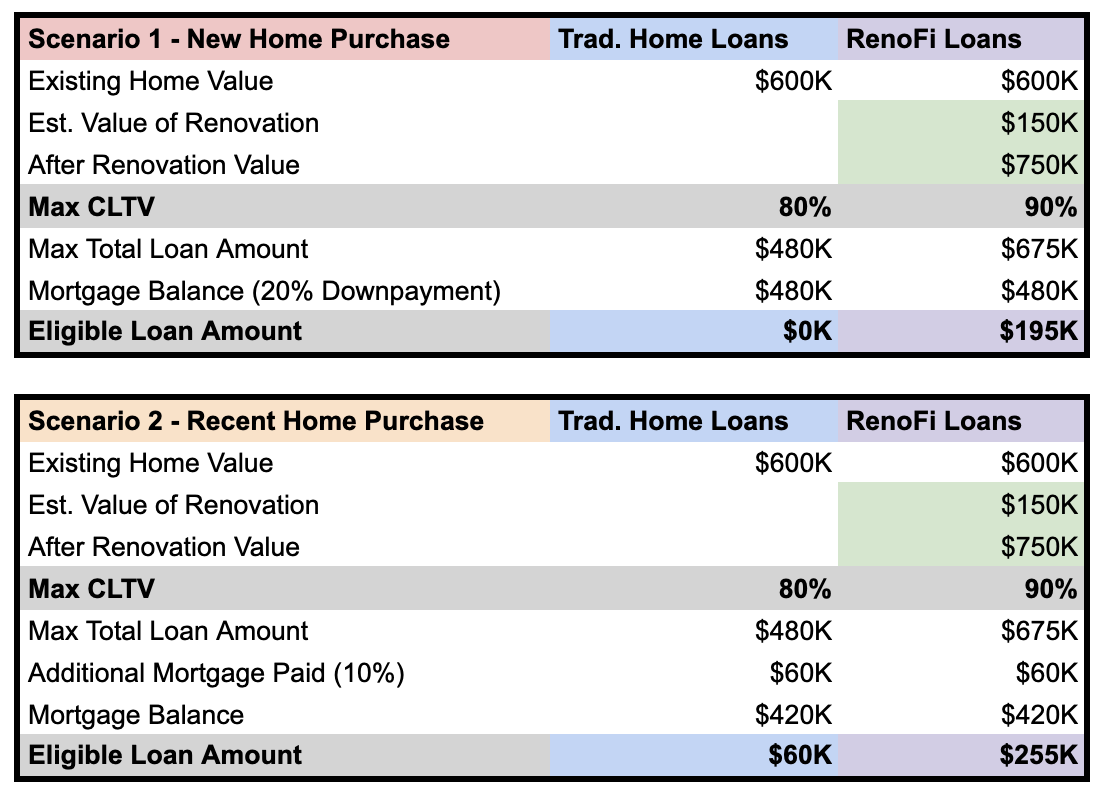

For example, let’s say you just purchased a home and you want to spend $150,000 to add an ADU or addition that you believe will add $150,000 in value to your home.

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to build your ADU or addition, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your ADU project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to build your ADU or addition, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereFinance Your ADU Project With a RenoFi Loan

When considering how to get a construction loan for your home addition or ADU, RenoFi loans might just be exactly what you need. They offer some of the best rates available, and you don’t need a ton of equity to qualify. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.