Getting a home improvement loan gives homeowners the opportunity to tackle costly projects around their homes and on their property. The loan could be the solution you’ve been looking for to do projects ranging from installing a second level to putting in new, beautiful and safe flooring.

When applying for any kind of home improvement loan, you can expect a thorough review of your financial health, including your credit score. Everything from the income you receive from any and all sources to your debt-to-income ratio will be evaluated.

How to Get a Loan for Home Improvements

A home improvement loan is a financing option designed to help homeowners fund their renovation projects, repairs, and property upgrades and improvements.

Make a checklist of the information you need to have available, some of which include:

- Tax returns

- Your credit score

- Detailed services estimate from a qualified, reputable contractor

- Employment history

- Proof of income

Steps for Getting a Home Improvement Loan

Now that you know what documentation the lender may request, it’s time to review the next steps in the process.

- Shop Around: Once you determine the exact loan you need, it’s time to shop around. You want to look at the rates, requirements, fees, and loan terms. All of these factors will ultimately affect the overall costs of your loan.

- Gather All the Documentation: Now, gather all the documents we mentioned. Depending on the lender, they may ask for more information.

- Prequalification: The prequalification process allows you to review your approval odds and doesn’t require a hard credit pull. You can do this with multiple lenders before you get into any official paperwork.

- Submit the Application: After comparing lenders, finish your application. Once approved, the lender will send you the documents you need to review and sign.

- Secure Funding: Once everything is signed, the lender will proceed with depositing the funds into your account so you can start your home improvement projects.

Borrowing Limits for Home Improvement Loans

There’s no guarantee when it comes to how much you can borrow for a home improvement loan, especially considering how many factors are involved. It’s important to ensure that the money you want to borrow aligns with the lender’s qualifications and guidelines, such as your credit score, for requesting that particular amount.

Homeowners can apply for high-dollar loans for major renovations. However, the higher the requested loan amount, the stricter the qualifications and the harder the home loan will be to get.

Remember, a home improvement project is typically anything aimed at enhancing the functionality, aesthetics, or value of your home, while major renovations are more geared toward restoring or repairing worn or outdated aspects of the home. Both are valuable.

- RenoFi Loans: While a traditional 80-85% LTV HELOC may sound like a viable option to fund a home renovation project, it often doesn’t work because the available equity isn’t enough to tackle your entire wishlist. One way to solve that is to take into account the After Renovation Value of your home and use that to increase the available equity - this is what RenoFi loans do.

- Personal Loans: These typically range between $1,000 and $100,000 and look at your credit score and history, income level, DTI ratio, and lender policies.

- Home Equity Loans: These generally range from 10% to 85% of the home’s equity. So, if your home is worth $500,000 and you owe $300,000, you have $200,000 in equity.

- Home Equity Lines of Credit (HELOCs): These are similar to home equity loans, where you can typically borrow between 10 and 85% of the home’s equity. Funds are withdrawn as needed up to a specific credit limit.

- FHA 203(k) Loans: The maximum loan amount is based on the home’s after-repair value (ARV), which can vary by region.

- VA Renovation Loans: The amount you can borrow is not limited, but it is influenced by the expected after-repair value.

- Cash-Out Refinancing: You can typically borrow up to 80-90% of the home’s equity. This option replaces your current mortgage with a new, larger one that gives you cash for renovations and home improvements.

Secured vs Unsecured Loans: Which Is Better?

An unsecured loan means there’s no collateral tied to it, whereas a secured loan uses collateral, such as your home’s equity. There are secured home improvement loans available and unsecured ones. You can use both for home improvement projects.

However, which one you should apply for depends on various factors. Research is crucial to determining which may be the best option for your financial situation.

Several elements determine which option is better for home improvement projects. Two primary factors are the size and cost of the projects.

Secured loans typically have lower interest rates than unsecured loans, which can be beneficial when you’re working with any amount, but especially large sums, such as those you need to complete major renovations and not just simple home improvements.

A secured home renovation loan may be an ideal fit, as it may offer lower interest rates. Depending on your equity and the size of the loan you want, you can use your home’s equity.

However, keep in mind that using your home’s equity as collateral also means you’re putting your home at risk for foreclosure if you can’t make the payments. There’s no risk of losing your home to foreclosure with an unsecured loan if you miss payments or you’re late, but expect a damaging hit to your credit score.

Home Improvement Loans for DIY Projects

Whether you can get a home improvement loan for DIY home projects depends on varying factors, such as the type of projects you want to do, your financial health, and the amount you’re requesting.

Many lenders prefer getting detailed cost breakdowns from professional contractors so they can see exactly where the money they’re loaning you is going and how it will be used. The professional title and licenses also help confirm that the work will be done as described.

While you can certainly apply for a home improvement loan if you want to do DIY projects, you’ll have to be willing to find the right lender who will be okay with that. You should also be prepared to provide an extensive breakdown of costs for each project and try to keep costs as low as possible.

Have a detailed plan ready to show how you plan on paying back the home improvement loan throughout its duration.

Renovation Project Planning

Once you determine the type of home improvement loan you want to use to fund your major renovations, be sure to define your goals and objectives, establish a realistic budget, develop a project timeline, and hire professionals to get the job done right.

When homeowners follow through with this level of preparation and renovation project planning, they can approach all large home renovation projects with more confidence and a clearer understanding of what’s required for the project’s success.

If you want to proceed with a kitchen remodel, bathroom renovation, or additional living space, consider RenoFi, a smart financing solution for all your bigger home renovation projects.

The Value of RenoFi for Home Improvements

RenoFi specializes in renovation loans, which allow homeowners to tap into the future value of their home after the improvements are made. Since the loan amounts are based on the after-renovation value, you can expect higher loan amounts. They are also much more accessible than other financing options like traditional loans or government-backed loans.

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

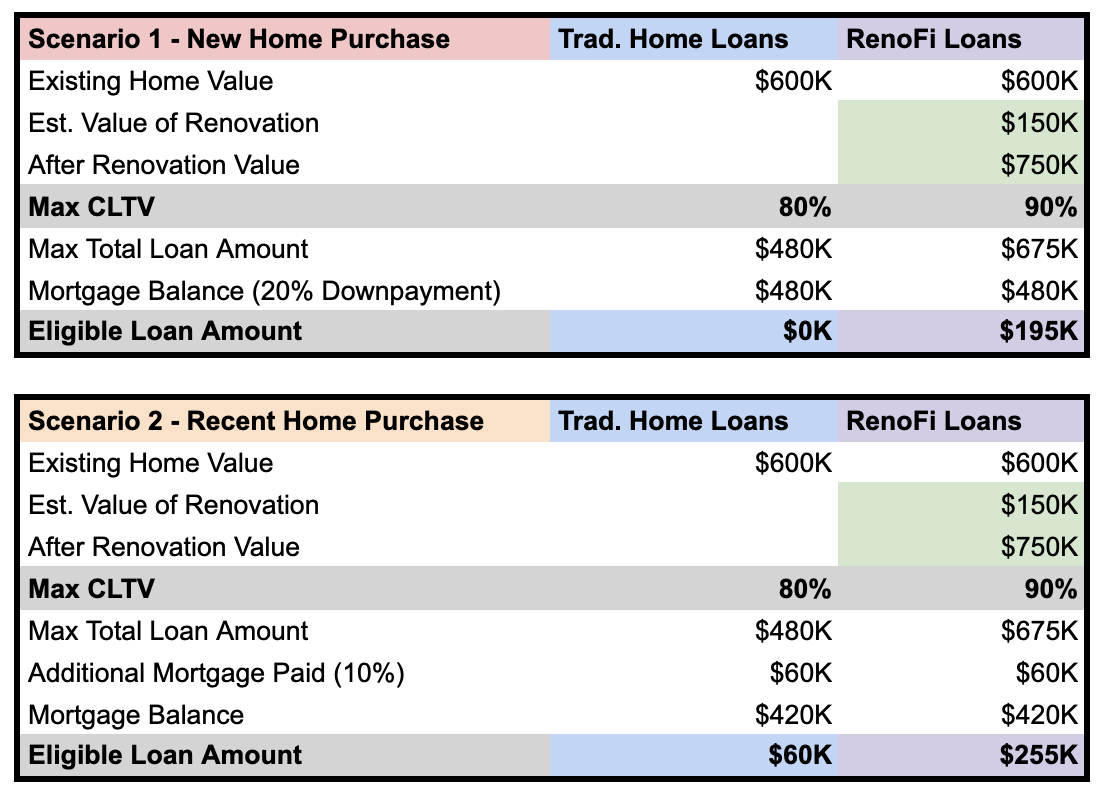

Let’s imagine an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

From finishing your basement to installing energy-efficient windows that can help you lower utility costs, you can use a home improvement loan in a variety of ways. RenoFi loans are the smartest way to finance a major home renovation project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80-85% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its after-renovation value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.