A home equity loan, or second mortgage, converts the equity in your home back into a loan. A second mortgage is a loan taken out against a property that already has a primary mortgage, using the home’s equity as collateral.

The money can be used for different things, such as debt consolidation and home renovation projects. The cash is received in lump sum payments with a fixed monthly payment and interest rate to be paid over an agreed period (5-30 years). This ensures a uniform and predictable payment plan, making it easy to budget for them.

Your Equity Explained

Your equity is the current value of your home less your outstanding mortgage debt. For instance, let us assume that your home is worth $500,000, and you still owe $400,000 on your mortgage. This means that you have $100,000 in equity.

Most lenders will allow you to borrow up to 80% of your home value. This means that your borrowing power is $0 since your outstanding mortgage balance equals the maximum amount you can borrow against your home equity.

Home Equity Loan Requirements

While each lender has their unique requirements, you will generally need:

- Your home equity to be at least 20% of your home’s current market value

- A credit score of more than 600

- Verifiable income history of at least 2 years

Difference Between Home Equity Loans and Home Equity Lines of Credit (HELOC)

Both home equity loans and HELOC loans are secured, use your home as collateral, and typically boast highly competitive interest rates compared to credit cards, personal loans, and other unsecured loans. However, these borrowing options have significant differences, including:

Loan Structure

Once you qualify for a home equity loan, you will receive the cash in a lump sum, while a HELOC loan allows you to withdraw your funds as needed.

Interest Rates

A home equity loan offers fixed interest rates which translate to a predictable monthly payment plan. On the other hand, HELOC loans come with varying interest rates which tend to vary with time, impacting your monthly payments.

Repayment Plans

Payment for a home equity loan starts immediately and is done over a pre-determined, fixed period, while a HELOC loan has a specific draw period during which borrowers are allowed to borrow and only pay interest. Then comes the repayment period, during which you must repay the loan in full, including the principal amount and interest.

Closing Costs

Due to its lump sum nature, a home equity loan might have higher closing costs than a HELOC loan, whose closing costs are typically lower.

Terms

A HELOC typically starts with a draw period, usually 10 years. During this time, the borrower makes interest-only payments. After the draw period, the loan enters the repayment period, which often lasts up to 20 years, and the principal and interest must be paid back. In contrast, a home equity loan usually has a fixed payment period, which can extend to 30 years, and the minimum payments include both the principal and interest from the outset.

Rates

A home equity loan typically has a fixed rate, which provides more predictable monthly payments, while a HELOC usually has a variable interest rate that can fluctuate based on current market conditions.

Borrowing Limits

The main difference in borrowing limits is that both usually allow homeowners to borrow between 80% and 85% of their home’s equity, though some lenders may offer more. The key distinction is that the home equity loan provides the lump sum upfront, while a HELOC offers a revolving credit line, which can be used as needed.

Pros and Cons of a Home Equity Loan

Now that you understand how a home equity loan works, let us explore its pros and cons.

Pros of a Home Equity Loan

- Possibly Lower Interest Rates:A home equity loan may offer significantly lower interest rates compared to a credit card or personal loan

- Fixed Interest Rates: Fixed interest rates provide a more predictable payment schedule and an easier way to budget

- Potential Tax Deductions: The interest on your home equity loan may be deductible if you use it for home renovation and improvement projects.

- Lump-sum Funding: Once you qualify, you will receive a large amount of money upfront, which you can use to fund large projects such as home renovations, debt consolidations, payment of emergency medical bills, and college fees.

- Improved Credit Score: Consistent, timely loan repayments prove to lenders that you are a trustworthy borrower, significantly improving your creditworthiness.

Cons of a Home Equity Loan

Risk of Foreclosure: You typically use your home as collateral to secure your loan. This means that defaulting payments can lead to the lender foreclosing on your home to recover your outstanding balance.

You can Only Borrow a Lump Sum: A HELOC loan allows you to borrow small amounts of money as needed, and only the interest on the amount you need to use. But with a home equity loan, you must receive your money as a lump sum all at once and then pay the interest on the entire amount. So, there is less flexibility.

Strict Qualification Requirements: As with any other loan, you must prove to your lender that you are capable of repaying your loan amount in full. You will, therefore, need to meet certain requirements, including:

- Debt-to-income ratio under 43%, depending on the lender

- Credit score of at least 620

- Home equity % of at least 15-20%

May Have to Pay Closing Costs: This can add additional upfront costs that can make the loan more expensive overall and reduce the immediate financial benefits.

Balance May Be Due: If you decide you want to sell your home before you have finished paying back the loan, then the balance of your home equity loan will be due.

Home Equity Loan vs Cash-Out Refinance

With a cash-out refinance, you replace your existing mortgage with a new, higher one, so you can have the difference in cash. When you do this, you will also get a new interest rate on your primary mortgage. This isn’t always going to be the ideal situation, however, because interest rates may be higher than before. You will also have to pay closing costs on the new loan.

A home equity loan is a second mortgage that allows you to borrow money using your home as collateral. It is separate from your original mortgage, so you will make two payments: one on your primary mortgage and one for the home equity loan.

While a traditional home equity loan might be a viable option to finance your project, it might not work if the home equity is not enough to tackle everything on your wish list. That is where RenoFi comes in.

RenoFi products such as RenoFi Home Equity Loan, RenoFi HELOC, and RenoFi Cash-Out Refinance are all based on the After Renovation Value of your home.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

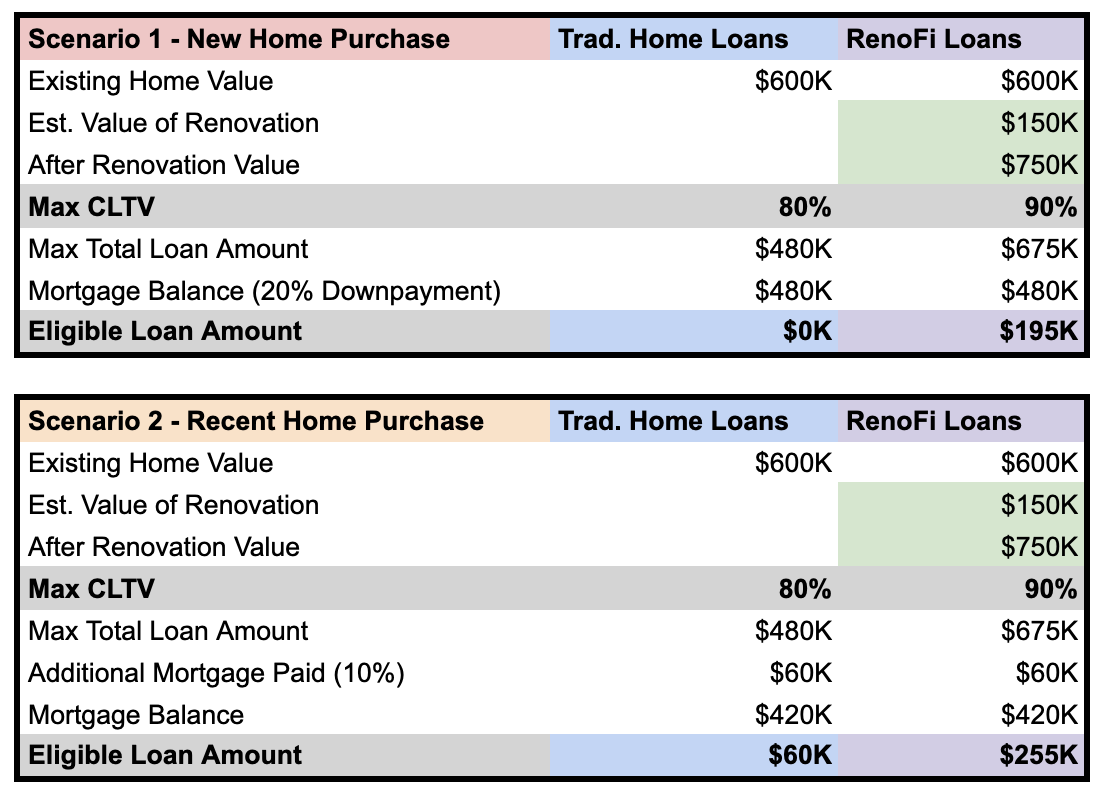

Scenario 1 (New Home Purchase): Let’s assume you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

By now, you understand how loan equity works and why a RenoFi loan is right for your home renovation project. Unlike most traditional loans, which are based on your current home value or require you to refinance your primary mortgage and potentially give up your low rate, RenoFi loans are more focused on the post-renovation value of your home.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.