Home rehab loans are designed to transform properties that need extensive updates or repairs to bring them up to the proper standards. This financing option helps homeowners or buyers pay for these extensive repairs, renovations, or improvements.

If you’re looking for financing to take on some major repairs in the near future, read on to learn more about the smartest ways to finance your efforts.

What Is a Home Rehab Loan?

While the terms home rehab loan and home renovation loan are generally synonymous, the idea of “rehabilitating” a house might paint the most vivid picture of the two.

A home rehab loan is about much more than a few coats of paint or a new rug: this type of financing can transform your property to make it more functional for your family (and more stylish).

Home rehab loans can be used to fund both a purchase and a renovation, or they can be secured on top of your existing mortgage when you decide it’s finally time to take the leap and transform your existing property into your dream home.

Types of Home Rehab Loans

Some of the common loans explored by homeowners as they plan to rehab houses include:

1. Federal Housing Authority (FHA) Loans

The FHA offers 203(k) rehab loans to homeowners in standard and limited offers. The standard 203(k) has a $5,000 minimum and is used for major renovations; the limited 203(k) cap at $35,000, so it may not cover a complete overhaul of a home in need of rehab.

While the FHA loans work well for some families, they also come with some exclusionary factors, including a minimum credit score requirement, a minimum 3.5% down payment, and a max on the homeowner’s debt-to-income ratio (43%).

If you are looking for help with a FHA 203(k) loan, RenoFi offers 203k loans through lending partners to help you find lenders for your property.

2. Fannie Mae and Freddie Mac Loans

Conventional rehab loans from Fannie Mae and Freddie Mac offer a little more flexibility than FHA loans. They allow homeowners to rehab a secondary residence or investment property. Similar to the FHA loan, these come with minimum credit score requirements, required down payments, and a 45% debt-to-income ratio.

3. Private Loans

A private or hard money rehab loan would include a shorter payment term and a higher interest rate, making them less attractive to the average homeowner. These loans are primarily used by real estate investors to get cash quickly, rehab the house, and sell it.

4. Personal Loans

These unsecured loans are ideal for small—to medium-sized home renovation and repair projects. You don’t have to have any collateral, but this also means they usually come with higher interest rates and shorter repayment terms. They are easy to apply for but are often limited to smaller amounts.

5. Home Equity Loans

A home equity loan is essentially a second mortgage. You borrow against your home equity for a lump sum of money you can use on large-scale renovation projects. They often come with fixed interest rates and more predictable monthly payments. However, they require sufficient home equity, and there is the risk of foreclosure if you fail to make the payments.

6. RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

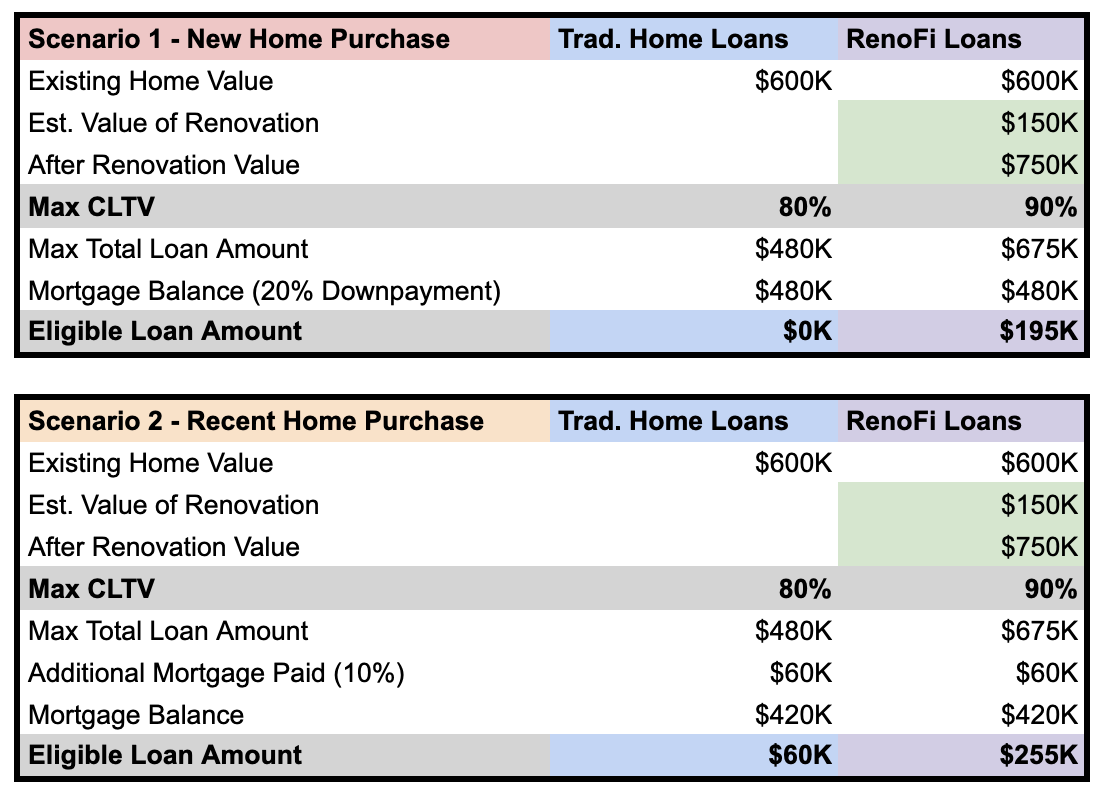

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Let’s imagine a scenario where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

6. Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit based on the equity in the home. This is a more flexible borrowing option that you can use as needed for phased or ongoing projects. You are only going to pay interest on the amount you borrow.

7. RenoFi Home Equity Line of Credit (RenoFi HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

8. Cash-Out Refinance

With a cash-out refinance, you can refinance your current mortgage and take out a loan for more than you owe. The extra cash can be used for home improvements. Cash-out refinances often have lower interest rates compared to personal loans, but you may be extending your mortgage term and will have higher closing costs.

9. RenoFi Cash-Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Eligible Property Types

Most rehab loans are available for single-family properties, which could be occupied or being purchased for renovations. However, the type of rehab loan also depends on the property. For example, eligible property types for FHA 203(k) rehab loans include owner-occupied properties being used as the primary residence, multi-family homes, condos, townhomes, and mixed-use properties.

Home rehab loans are designed to support homeowners looking to renovate and improve their primary residences. However, specific guidelines do apply to the type and scope of the renovations and the property type, as you can see.

The Pros of Home Rehab Loans

Rehab loans can be an attractive option for many due to a few of these key features:

- Higher Loan Amounts: Rehab home loans often offer more than traditional loan options do. This puts more money in your pocket for larger renovation costs.

- More Flexible With Eligibility: Rehab loans are often more accessible to borrowers, even those with less-than-ideal credit scores or limited incomes.

- More Streamlined: You can typically find a much more streamlined application process for these loans with faster turnarounds and a bit less paperwork than other financing options might require.

- Covers Purchase and Renovation: Home rehab loans, like an FHA 203(k), allow you to combine the cost of buying a home with necessary renovations.

- Leverage Future Home Value: RenoFi loans, for example, let you borrow based on the after-renovation value of your home. This allows you to borrow more than a traditional loan based on current equity.

- Lower Down Payment Requirements: Some of these loans, like FHA, often require lower down payments and this makes them accessible to more homeowners.

The Cons of Home Rehab Loans

Home rehab loans provide homeowners with valuable financing options for renovations, but there are some potential drawbacks to be aware of.

- Higher Interest Rates: Depending on the type of rehab loan, interest rates could be much higher than a traditional mortgage or home equity loan.

- Market Fluctuations: A declining housing market may make the value of your home drop below the loan amount. This leads to negative equity and can make it harder to sell or refinance.

- Post-Renovation Appraisal Requirements: The lender may want an inspection after all the renovations are completed. This can cause delays and disputes.

- Potential for Excessive Debt: Borrowing against your home’s future value could lead to higher debt levels if the renovations don’t increase your home value.

- Strict Guidelines: Some of these loans have more stringent guidelines that limit the types of projects and improvements that are eligible. Some also require that you use approved contractors.

RenoFi for Smart Financing

Researching and applying for loans can be overwhelming for even longtime homeowners who are experienced with mortgages and home renovations. In many cases, the dreams of a home rehab are quickly crushed when a qualifying factor is out of reach.

RenoFi is committed to guiding homeowners in this process, and we offer something unique based on your home’s after-renovation value (ARV). Our strategy is built upon determining what your home may be worth after the rehab, not before, and putting that borrowing power in your hands up front.

Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.