Although home loans aren’t an official term or category, they typically refer to loans that offer financing for buying, building, or renovating a property, with the property itself as collateral for the lender. However, there are some loans you can get that don’t require you to use your home as collateral at all.

Navigating home loan options can be daunting due to the complex terminology and various financing products available. Home loans vary, so knowing which type suits your needs best helps you negotiate effectively with lenders for the optimal deal.

Different Loan Types

Home loans (also known as mortgages) can be categorized in various ways depending on their features. While most types of these mortgages finance the purchase and renovation of properties, they can be roughly divided into government-backed loans and conventional loans.

1. Traditional Home Equity Loan

Many homeowners choose home equity loans to finance their renovation projects and borrow against the equity they’ve built in their homes using a second mortgage.

Equity is the difference between your home’s current market value and your outstanding mortgage balance. A home equity loan provides a lump sum that you repay over time with fixed monthly payments and a set interest rate.

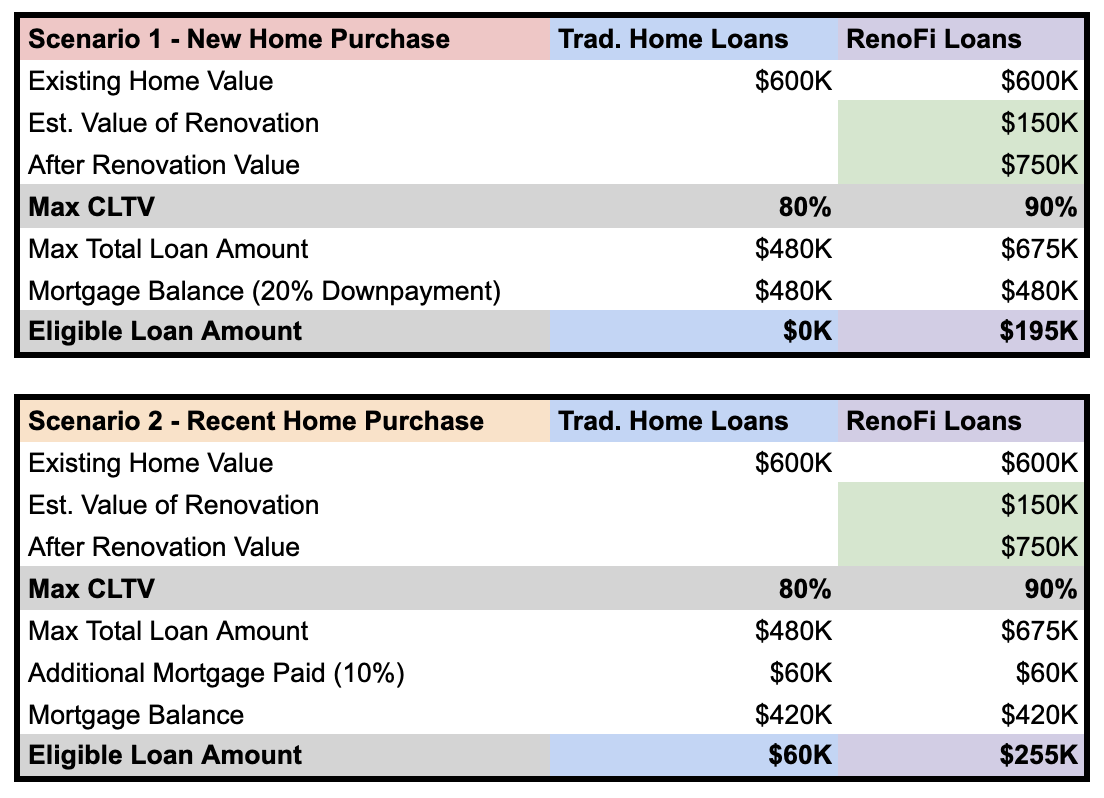

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home Price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home Price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

2. RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Using the same example above:

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home Price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Traditional Home Equity Line of Credit (HELOC)

Just like a credit card, you can borrow money with a HELOC up to a pre-approved limit, but the equity in your home backs it. HELOCs have variable interest rates and let you draw funds as needed, making them ideal for long-term or ongoing renovation projects.

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home Price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home Price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

4. RenoFi Home Equity Line of Credit (RenoFi HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home Price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

5. Cash-Out Refinance

A cash-out refinance replaces your current mortgage with a new mortgage that is greater than what you currently owe with a different interest rate and payment amount. Unlike Home Equity Loans, a Cash Out Refinance is a brand new loan with a different interest rate rather than a second loan on top of your existing loan.

Scenario 1 (New Home Purchase): Using the same example above

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home Price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Cash Out Refinance % of Home Price: 80%

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

6. RenoFi Cash-Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home Price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home Price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

7. Conventional Mortgage Loan

The most prevalent option is a conventional mortgage or home loan, which is provided by private lenders like banks and mortgage companies rather than government agencies.

To qualify, borrowers typically need a credit score of 620 or higher, a down payment of at least 20% (with private mortgage insurance required if less), verifiable income for the past two years, and a debt-to-income ratio of 43% or lower.

8. FHA Home Loan

Government-backed loans feature insurance from a federal entity that secures different loan types. These programs generally have more accommodating down payment and credit score standards, allowing more homebuyers to qualify.

An FHA home loan, insured by the Federal Housing Administration and issued through approved lenders, is ideal for first-time buyers and those with limited income due to its lower down payment and credit score requirements. While borrowers must pay mortgage insurance, which is about 1.75% of the loan amount, the program offers benefits like reduced qualification standards and affordable insurance.

Applicants need a credit score of at least 500 with a 10% down payment or 580 with 3.5% and must meet income and property criteria. FHA loans can be more affordable for those with lower credit scores or smaller down payments but may be pricier for those with good credit and larger down payments than conventional loans. Comparing lender quotes can help find the best deal.

9. VA Home Loan

A VA home loan, backed by the US Department of Veterans Affairs, allows veterans, active-duty service members, National Guard and reserve members, and surviving spouses to buy homes with minimal to no down payment and competitive interest rates.

Moreover, they do not need to sign up for private mortgage insurance. While the VA sets the loan standards and guarantees, private lenders handle the financing. Eligibility requires a Certificate of Eligibility, meeting service requirements, and a verifiable employment history.

VA loans offer benefits such as flexible guidelines, no fixed credit score requirements, and limited closing costs, as well as assistance to prevent default. They might be more costly than conventional loans if you have a significant down payment and good credit, but they are ideal for those with limited funds and needing favorable terms.

10. USDA Loans

The US Department of Agriculture offers a financing option for individuals with modest incomes in rural areas, comparable to FHA and VA programs. These USDA loans are particularly beneficial for those with minimal savings, as they do not demand a down payment and generally have lower costs than FHA loans. Nonetheless, borrowers are responsible for an initial fee and continuous mortgage insurance premiums paid to the USDA.

11. Personal Loans

Personal loans are unsecured loans and don’t use your home as collateral. They can be used for various purposes, including debt consolidation (e.g. replacing multiple debts with one), home improvements, major construction purchases, and unexpected costs. Interest rates can range anywhere from 7% to 36% (as of October 2024).

Typically, borrowers receive a lump sum of $1,000-$100,000, which they repay in fixed monthly payments over one to seven years. However, with Renofi loans, you can extend the repayment period up to twenty years to make budgeting easier for your renovation projects. With a RenoFi personal loan, you can get up to $100,000 in funding with a 20-year term and competitive rates.

Personal loans are flexible and available through banks, credit unions, and online lenders. Eligibility is mostly based on credit score and a manageable debt-to-income ratio. They are ideal for covering the expenses involved in home renovation projects and remodels without delay.

Loan Basics

Most families purchase homes with a mortgage that covers part of the property’s cost. When shopping for a mortgage, key terms to understand include the loan term, often 30 years but available in shorter durations, and the down payment, which is a percentage of the home’s price required upfront. Interest rates, which can be fixed or adjustable, determine the cost of borrowing.

Payment frequency is typically monthly, with fixed and adjustable-rate mortgages having payment schedules that fully amortize the loan over time. Mortgage types vary based on loan size and government involvement, affecting the down payment amount, total loan cost, and borrowing capacity.

For example, government-backed loans like those from the FHA, VA, and USDA often require low down payments compared to more conventional loan options. Choosing the right mortgage type involves comparing options and quotes from lenders to find the best overall deal.

Understanding How Mortgage Loans Function

In the primary market, lenders extend loans to borrowers to purchase homes. These loans, commonly known as mortgages, are offered by various institutions, including banks, credit unions, and finance companies specializing in lending.

When a borrower applies for a mortgage, the lender undertakes a thorough underwriting process to evaluate the borrower’s financial situation and creditworthiness.

The secondary mortgage market is a vast domain where various entities trade mortgage loans and servicing agreements. This sector features diverse participants, such as investors, loan providers, aggregators, and financial brokers.

Credit Score

Your credit rating dramatically impacts your chances of obtaining a mortgage. Higher ratings typically result in more straightforward approvals, reduced down payments, and more favorable rates.

For example, an individual with a credit rating of 760 might obtain a $200,000 mortgage at a 3.6% interest rate, leading to monthly payments of $910.64 and a total interest cost of $127,830 over 30 years. In contrast, a rating of 635 could result in a higher rate of 5.2%, causing monthly payments of $1,098.35 and a total interest expense of $195,406.

Mortgage Trends

According to recent US Census Bureau data, between 2017 and 2022, 61.5% of homeowners had a mortgage, with 53.7% holding only a primary mortgage, 6.6% having multiple mortgages, and 38.5% being mortgage-free.

The fixed-rate, 30-year mortgage is the most popular home loan in the US, with many homeowners opting to repay it over thirty years.

Homebuyers or those refinancing can opt for shorter loan terms, such as 15 or 20 years, instead of the typical 30-year mortgage. These shorter terms build equity faster and reduce the total interest paid; for instance, a $250,000 fixed-rate mortgage in 2017 would cost about $168,000 in interest over 30 years but only $62,000 over 15 years.

However, shorter-term loans come with higher monthly payments—up to 40% more for a 15-year mortgage—which might limit the price of the home you can afford. Additionally, making extra payments on a mortgage can accelerate equity buildup and shorten the loan term; for example, adding $100 extra monthly to a $225,000 30-year mortgage can cut the term by over four years.

Conclusion

While traditional home equity options rely on current property value, RenoFi loans provide a unique advantage by utilizing the projected value post-renovation. This approach can significantly enhance borrowing power, especially for new homeowners or those with limited equity.

The more equity you’ve built up, the more cash you can get with a HELOC loan. But even if you don’t have a lot of equity, RenoFi’s unique offer can help. With a RenoFi HELOC, you can actually borrow more than a traditional one would allow. This option lets you take out up to 125% of your home’s future value after renovation, even before you start renovating. In other words, you can secure a loan based on what your home will be worth once the upgrades are finished.

If you’re planning to make some improvements to your home, RenoFi loans are the smartest way to finance a home renovation project. Unlike traditional loans, which are based on your current home value or require you to refinance your primary mortgage and give up your low rate, RenoFi loans are based on the After Renovation Value of your home. This allows you to borrow on average 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Don’t hesitate to reach out if you’d like to learn more about the RenoFi HELOC or have any questions about using your home equity for improvements.