Home equity and HELOCs both allow homeowners to turn their home equity into cash using property as collateral and offer better interest rates than standard credit cards, personal loans, or other unsecured debts.

While both home equity loans and HELOCs (home equity line of credit) use the home’s equity value, they aren’t the same. Understanding the difference between home equity and HELOC is crucial to deciding which option is right based on your financial needs and goals.

In this article, we will compare home equity loans with HELOC to help you decide which financing option will benefit you most based on your situation.

What Is Home Equity?

Before getting started, let’s talk about home equity and how to calculate it. Home equity refers to the difference between the market value of your property and the debt you have on any liens. For example, if your home is worth $600,000 and your principal mortgage balance is $200,000, your build-up home equity is $400,000.

Equity fluctuates as you make monthly mortgage payments and the property’s market value changes. Home equity loans and HELOCs allow you to access a substantial portion of this equity to work on major and minor projects.

What Are Home Equity Loans?

Home equity loans, or second mortgages, provide the borrower with a one-time lump sum. The bank or lenders usually offer them and let you borrow 75 to 90% of the home equity by putting the home and property up as collateral. It is typically based on your loan-to-value (LTV) ratio. For example, if a lender allows up to 85% LTV, then you can borrow 85% of the home’s value minus your primary mortgage.

Home equity loans have a fixed interest rate based on your income, debt, and credit score. The loan contract also states the repayment period, which may last 5 to 30 years.

Equity loan payments are stable and made monthly, making them easy to budget. They are ideal for funding large, one-time projects such as debt consolidation, home remodels, and down payments for other investments.

However, if you cannot pay off the debt or default by missing payments, the lender has the legal right to take ownership of your property. This is known as foreclosure, and in severe cases, it may require you to sell the entire property to pay off the borrowed amount.

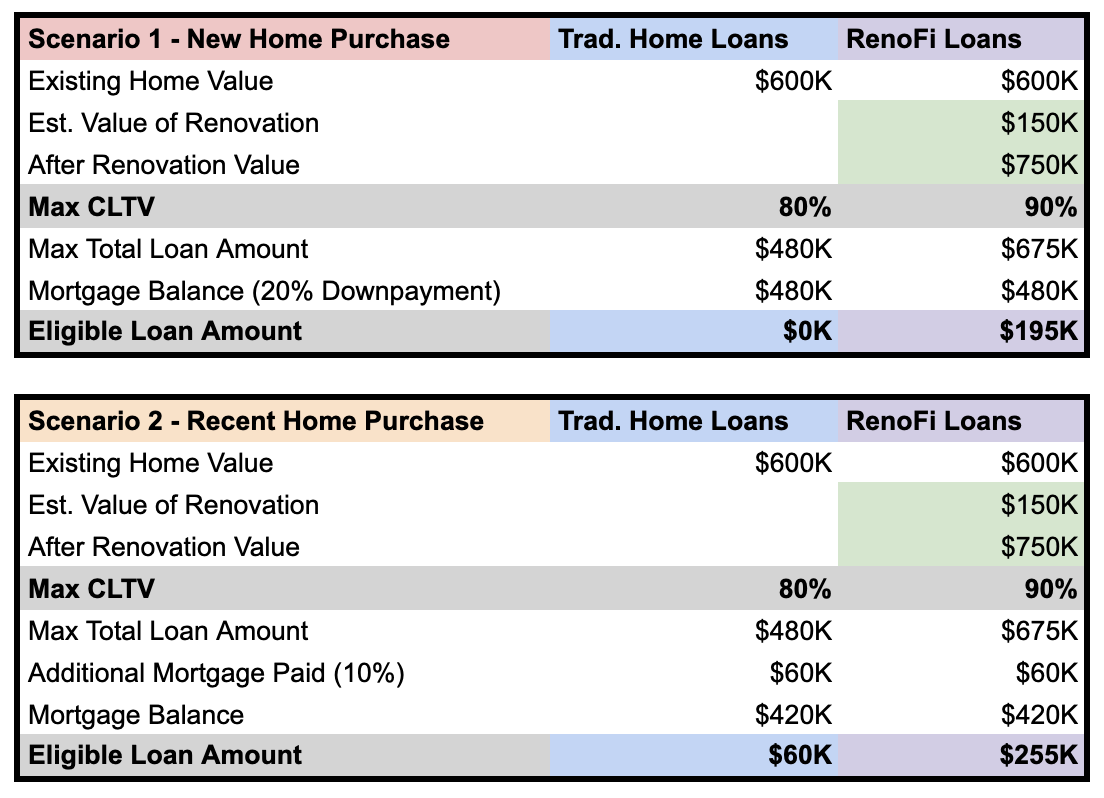

Scenario 1 (New Home Purchase): Let’s look at an example, and to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Using the same example above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

What Are Home Equity Lines of Credit?

Like standard equity loans, home equity lines of credit (HELOCs) are also secured by your property. However, they work as revolving lines of credit rather than a one-time payout. With HELOCs, borrowers can access funds up to a specific credit limit, which they can use or reuse as needed.

The draw or borrowing period often lasts ten years, and once it is over, the repayment period starts. After this period, the borrower no longer has access to the money and makes monthly payments, including the principal and interest, to pay off the debt. Moreover, various lenders offer an interest-only HELOC. If you opt for that option, you only pay interest but no principal amount during the draw period, typically ten years.

The repayment period may last between 10 and 20 years, depending on the amount owed. Unlike home equity loans with fixed interest rates, HELOCs charge variable interest rates, initially decided based on your creditworthiness. Additionally, borrowers need to pay interest only on the money they use.

Due to their flexibility, HELOCs are ideal for financing ongoing home renovation projects and making emergency long-term expenses or tuition payments. However, due to their possibly high, variable interest rates, they also involve the risk of paying much more than you owe.

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

RenoFi Home Equity Line of Credit (RenoFi HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Home Equity Loan vs HELOC - What’s the Difference?

Home equity loans and HELOCs are smart financing strategies that allow you to fund major ongoing renovation projects and investments. To pick the right option for you, consider the following factors:

Withdrawal Amount

Home equity loans provide a lump sum of money at once. Banks and lenders use formulas such as the LTV ratio to determine the build-up equity on your house and let you borrow a percentage of the total value. A HELOC, however, allows multiple withdrawals up to a set limit over an extended period.

While a traditional 80% LTV HELOC sounds like a suitable option to fund a renovation project, it usually doesn’t work because the available equity isn’t enough to cover the involved expenses. A possible solution for this is to consider the After Renovation Value of your home and use that to increase the available equity.

This is precisely what RenoFi loans do. We focus on the after-renovation value to allow you to borrow as high as 125% of your current home value or 90% of its future value, offering immense borrowing power regardless of your home’s current equity.

Interest Rate

Home equity loans have a fixed and significantly lower interest rate than other loans. Alternatively, HELOCs feature variable interest rates prone to rise if the market value increases. With HELOCs, there’s a greater risk of defaulting and foreclosure than with the standard equity loan.

Repayment Period

The repayment period for home equity loans typically lasts 5 to 30 years. During this time, the borrower is required to make fixed monthly payments. Meanwhile, HELOCs are divided into separate draw and repayment periods. The monthly payments are comparatively higher and may require as much as 20 years to be repaid.

Conclusion

Home equity loans and HELOCs each have unique benefits and drawbacks. Consider various factors, including your project’s expenses, income, and current home equity, to decide which financing option works best for you.

RenoFi is dedicated to providing you with the necessary resources and education needed to make your financing decisions. Our RenoFi loans offer the smartest way to finance major home renovation projects. Unlike traditional loans, which are based on your current home value and require you to refinance your primary mortgage and give up the low rate, RenoFi loans consider the after-renovation value of your property.

RenoFi offers, on average, 11 times more borrowing, low monthly payments, and a low rate on your first mortgage. Whether you opt for a home equity loan or HELOC, browse RenoFi loan options and get started immediately.