Home equity loan guidelines refer to the criteria and rules lenders use to determine whether a borrower qualifies for a home equity loan and how much they can borrow. If you own a home, a home equity loan could be a way to get money by using the value of your property.

In this article, we’ll explore the essential guidelines for home equity loans while also introducing RenoFi loans, a smart and innovative alternative designed specifically for homeowners looking to finance large-scale renovations without refinancing or losing their current mortgage rate.

Essential Facts About Home Equity Loans

A home equity loan is a type of loan in which a homeowner borrows against the equity in their home. The more equity you have in your home, the more you can borrow. As you continue to pay down your mortgage, the more your home’s value increases, the higher your equity will be. So, if your home is worth $300,000 and you owe $200,000, you have $100,000 in equity.

With a home equity loan, you typically have a fixed interest rate and repayment term, meaning you’ll make the same monthly payment throughout the life of the loan. This predictability appeals to homeowners who budget for major expenses. People commonly use home equity loans to cover major expenses like renovations, medical bills, or educational costs.

Key Guidelines for Home Equity Loans

Before you take out a home equity loan, there are several key factors to remember. These guidelines will help you better understand the terms, eligibility requirements, and responsibilities of this type of loan.

1. Proof of Income

A lender requires proof of income as a way to assess your ability to pay off a loan. To show consistent and verifiable income, you will need to show recent pay stubs, W-2 or 1099 forms, tax returns for the last two years, and bank statements showing income deposits. If you have other income streams—like rental income or investments—make sure to include those as well, as they can strengthen your application.

2. Homeowner’s Insurance

A lender will also require proof of homeowner’s insurance. This shows them the property is protected, which is important since the property serves as collateral for this kind of loan. You will need to show them your current homeowner’s insurance policy or declaration page and proof of sufficient coverage.

3. Loan-to-Value Ratio (LTV)

Your home equity determines how much you can borrow. The amount you can borrow is usually 80% of your home’s value, minus your current mortgage balance.

The higher your equity, the more you can borrow, but staying within your means is essential. Be careful not to borrow too much, as it could lead to higher monthly payments and make it harder to manage your finances.

4. Credit Score Requirements

Just like with most types of loans, your credit score plays a significant role in determining eligibility and loan terms. In most cases, lenders look for a credit score of at least 620 to 640 to approve a home equity loan.

However, higher credit scores often result in more favorable interest rates and terms. If your credit score is on the lower end, improving it before applying may be beneficial to secure better loan conditions.

5. Debt-to-Income Ratio (DTI)

Another crucial guideline to consider is your debt-to-income (DTI) ratio. Your DTI ratio measures how much of your income is spent on paying your debts, such as your mortgage, car loans, credit cards, and other bills.

Most lenders require a DTI ratio of no more than 43% to qualify for a home equity loan. Lowering your debt before applying for a loan can improve your chances of approval and possibly help you secure a better interest rate.

6. Payment History

A lender may examine your payment history to further evaluate your creditworthiness. A strong payment history shows that you are more likely to make timely payments on a new loan. The lender will pull your credit report and will look at your mortgage payment history as the lender wants to see a history of on-time payments.

7. Interest Rates

Because they’re secured by your home, home equity loans generally have lower interest rates compared to personal loans or credit cards. However, these rates can vary based on several factors, including your credit score, the loan amount, and the lender’s policies.

Therefore, when looking for a home equity loan, it’s worth comparing different lenders and finding the best deal. Even a small difference in interest can make a big impact on the total cost of the loan.

8. Closing Costs and Fees

Just like your primary mortgage, a home equity loan comes with closing costs and fees. These costs can range between 2% and 5% of the loan amount, covering appraisal, title search, and attorney fees.

While some lenders may offer no-closing-cost loans, these usually have higher interest rates. When deciding on a loan, compare total loan costs, not just the interest rate.

9. Tax Implications

Interest paid on home equity loans may be tax-deductible if the funds are used for home improvements. However, the interest may not be deductible if you use the funds for personal expenses, such as paying off credit card debt. Since tax laws can change, it’s crucial to consult with a tax professional to understand your situation.

Understanding RenoFi Loans as an Alternative

While traditional home equity loans can be beneficial, they may not always be the best option, especially for larger renovations or projects. RenoFi loans are designed to address some of the limitations of traditional home equity loans.

The RenoFi Advantage

While traditional home equity loans provide access to your home’s current value, they may not be ideal if you plan on undertaking a major home renovation.

Traditional home equity loans are limited by your home’s current value, which can be a drawback for major renovations. RenoFi loans, however, let you borrow based on your home’s future value after renovations, offering a better solution for large projects.

Let’s look at a couple of simple examples where you want to spend $150,000 to renovate your new home and increase the value of your home.:

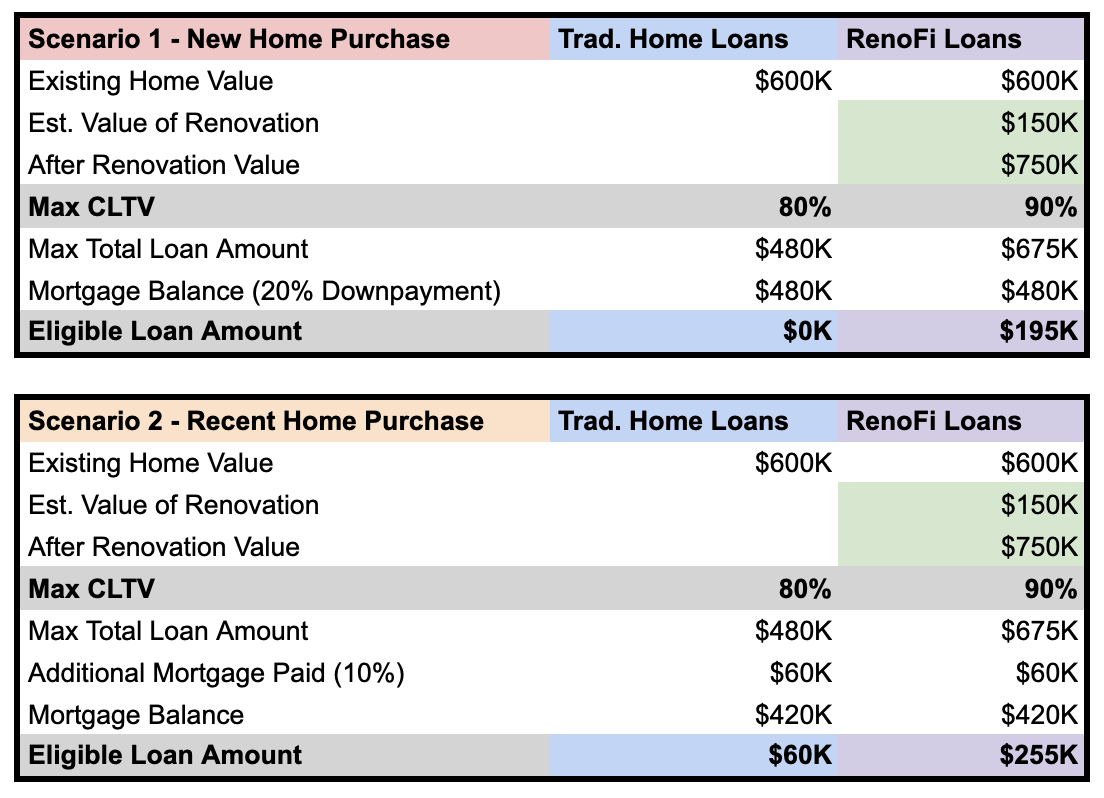

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

For instance, if your home is worth $500,000 with a $400,000 mortgage, a standard loan wouldn’t provide extra funds due to the 80% loan-to-value limit. With RenoFi, if renovations increase your home’s value to $640,000, you could borrow up to 90% of that value. This allows homeowners to access more funds without refinancing or losing their low mortgage rates.

Get started with your RenoFi loan hereChoosing the Right Home Equity Option

When deciding between a traditional home equity loan and a RenoFi loan, It’s important to weigh the pros and cons of a traditional loan versus a RenoFi loan based on your needs and financial situation:

- Loan Purpose: If your project requires substantial funding, a RenoFi loan may be the best choice due to its higher borrowing capacity.

- Interest Rates: Most importantly, remember to compare interest rates and terms from different lenders to find the most favorable options.

- Financial Flexibility: Lastly, consider how a home equity loan or RenoFi loan aligns with your long-term financial goals.

Conclusion

If you want to leverage your property’s value, home equity loan guidelines are crucial. Understanding eligibility criteria, types of loans, and associated costs can help you make informed decisions. However, if you’re considering a home renovation or large project, exploring options like RenoFi loans can provide additional benefits, such as higher borrowing limits based on your home’s future value.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.