A hard money rehab loan is a short-term financing option primarily used by real estate investors looking to purchase and renovate properties.

However, if you are a home owner who wants to borrow money to renovate your own home to increase the value of your home, RenoFi allows you to borrow against the after renovation value of your home to borrow up to 11x more on average.

Hard money rehab loans are specifically designed for flip-and-fix scenarios, where the investor can turn a profit and are usually provided by private lenders or investment groups instead of traditional banks.

Benefits of Hard Money Rehab Loans

Using hard money loans to finance your real estate capitalization allows you to access funds relatively quickly, which is good in a competitive market. Here are the benefits of hard money rehab loans:

- Quick Financing: This loan process finalizes quicker than conventional loans due to the private financing aspect. The credit score, your finances, and employment status don’t determine the approval of the financing. These loans focus on the value of the property and not the borrower’s credit history.

- Less Strict Requirements: Hard money rehab loans have more flexible terms and structuring.

- Covers Rehab Costs: These loans can cover the purchase and renovation expenses while giving investors more capital for their projects.

Cons of Hard Money Rehab Loans

While there are some advantages to this kind of loan, you should also be aware of its drawbacks. They are not meant for homeowners wanting to stay on their property for the long run. You will want to look into other financing options if you want to take on major home renovations to improve your home such as RenoFi loans.

- Higher Costs: Hard money rehab loans often have higher interest rates and fees, which can make them much more expensive in the long run.

- Shorter Repayment Terms: Borrowers need a clear repayment plan, whether through refinancing or selling the property as quickly as possible.

- Risk of Foreclosure: If the borrower fails to repay the loan, the lender can then seize the property.

- Limited Availability: Not all lenders offer hard money loans, and if they do, there are specific criteria that need to be met

- Overvaluation: Lenders may overestimate the ARV, which can lead to borrowers taking on more debt than the property can actually support.

Hard Money Rehab Loan Terms

Hard money rehab loans are usually not accessible at all financial institutions due to their stringent application processes. The repayment period for these loans can be between three months and three years. The lender assesses the property’s value and anticipated renovations and compares it with homes in the area to evaluate the value after rehab.

Tips for Accessing the Best Hard Money Rehab Financing

- Find reputable lenders with positive reviews.

- Understanding the interest rates, repayment periods, and any additional charges and loan terms helps you choose your ideal rehab loan.

- Have a home renovation and financing repayment plan in place to showcase the project’s benefits and simplify the financing process.

What to Know About Hard Money Financing

Hard money financing differs from traditional financing options and aren’t designed for the typical homeowner, so it’s important to understand these key points:

- Interest Rates: The interest rates are usually higher because the loan approval process doesn’t involve conventional checks. This increases the lender’s risk, which often translates to higher interest charges.

- Financing Period: This financing option is often shorter than other loan types

- Loan Approval Criteria: Conventional lenders approve financing using normal criteria such as debt-to-revenue ratios and credit checks. For hard money rehab funding, the lenders typically apply their own terms and conditions.

- Potential for Foreclosure: Since the property serves as collateral for these loans, failure to meet all loan terms can result in foreclosure.

Loan Application Process

Accessing hard money rehab financing is easy and quick. Here is the process explained:

- Pre-qualification and Application Stage: You can get a pre-qualification with a suitable lender or submit a free financing analysis. Unlike conventional financiers, hard money lenders don’t focus on your credit rating but on your property value.

- Expect a seamless loan application process with a shorter repayment timer and a potentially quicker approval rate.

- The disbursement usually happens in stages to provide effective property renovations. If you intend to improve your property value, notably, a hard money rehab loan is ideal since it is determined by the property’s after-repair value (ARV).

What Is Required for a Rehab Loan?

To obtain a hard money rehab loan, you need the following items before engaging with a lender:

- Buying Contract: If you are buying a degraded property that requires rehabbing, the lender will need to see a purchase agreement.

- Rehab Costs: You must provide the lender with repair costs and any rehab-related bills calculated by the contractor.

- Asset Pictures: You should provide detailed and clear photos showing the areas that require rehabbing and updating. This will help the lender understand your project requirements.

- Loan Request: Although not all hard money rehab loans require applications, you must provide core personal information and property information to be able to secure the loan amount you need.

- Proof of Security: Some lenders will need insurance against hazards before they can approve your hard-earned rehab loan.

Benefits of RenoFi Loans

Are you a homeowner who wishes to stay in your home for the long term? Maybe you have been compiling a list of major home renovation projects you want to start checking off to improve the space, comfort, or livability of your home.

Let’s compare how RenoFi loans stack up against traditional home equity loans. Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

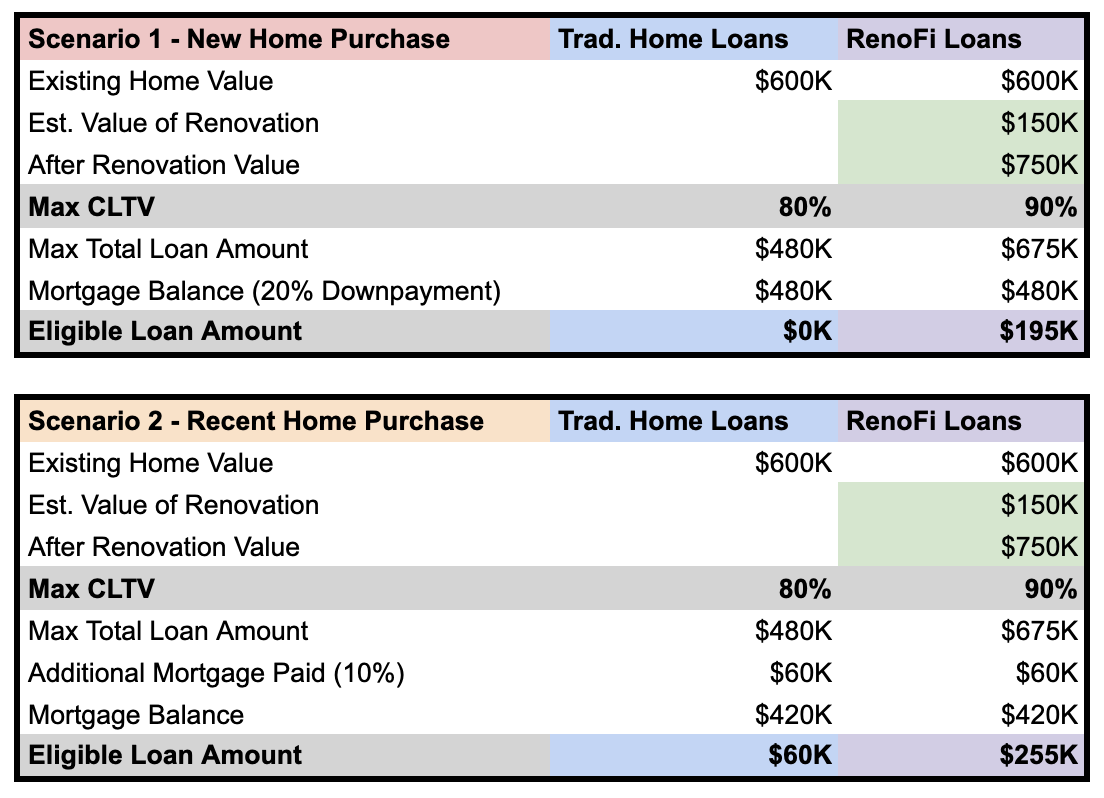

Scenario 1 (New Home Purchase): Using the same example above where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

RenoFi loans are the best way to fund any major home renovation project you have in mind. Unlike conventional loans that calculate your financing based on the current home value, RenoFi financing is calculated by the after-repair value to allow you 11x low-interest rate loans.

If you need a loan that is a much better fit for a homeowner looking for potentially lower-cost, longer-term financing, consider RenoFi.