A construction loan for remodeling is a type of financing that helps homeowners tackle renovations and improvements to their homes. If you’re planning to make some significant changes, this could be a great option. However, there are specific details you should know before jumping in.

What Is a Construction Loan and How Does It Work?

A construction loan is a short-term loan specifically created to help cover the costs of building or renovating residential properties.

These loans typically work a bit differently than traditional mortgages. Instead of receiving all your funds upfront, your lender will disburse the money in stages based on how far along your project is. This means you’ll get cash as you hit specific milestones, such as finishing the framing or completing electrical wiring.

This approach can ensure the funds are used correctly and your project stays on track. It also means you’ll need to keep your lender updated on your progress so they can release the next round of funding.

Common types of construction loans include:

- Construction-only loans: These cover only the construction costs and must be paid off once the project is completed.

- Construction-to-permanent loans: These construction loans convert to a standard mortgage once the building is complete, also helping with the acquisition of a property or land and the actual build.

Can You Use a Construction Loan for Remodeling?

Even though construction loans are mainly for new builds, you can use them for major renovations as well. In some instances, they can also help with borrowing power because they leverage the After Renovation Value.

One alternative to using a construction loan is a RenoFi loan as it also uses After Renovation Value but it sits in second lien position so you don’t need to give up your first mortgage and the rate you have. Unlike construction loans, RenoFi loans don’t require draws and inspections, instead, they’re funded to the homeowner in full upon closing.

How to Qualify for a Construction Loan for Remodel

To get approved for a construction loan for your remodel, there are a few things you’ll usually need:

- A credit score of at least 620

- A reasonable debt-to-income ratio (generally below 45%)

- A sizable down payment (often up to 20%)

- A detailed construction plan and timeline

- A contract with a licensed builder or contractor

How to Apply for a Construction Loan for Remodel

Here’s how to apply for a construction loan for your remodel:

- Research Lenders: Look into different lenders and their construction loan options to find one that suits your needs.

- Gather Your Documents: Get together all necessary documents, including proof of income, credit reports, and a detailed project plan with contractor bids.

- Submit Your Application: Choose a lender and send in your application along with all the required paperwork.

- Work With Your Lender: Once approved, stay in touch with your lender throughout the construction to ensure payments are made to your contractors on time.

Key Considerations for a Construction Loan for Remodeling

Alternative Loan Options

Before taking out a traditional construction loan, consider a RenoFi loan, which can be a simpler and faster solution for remodeling or renovating a property.

Construction loans require a full refinance and are based on the current value of your home. They also involve more complex draw schedules and inspections, which can add time and complexity to your project.

In contrast, RenoFi loans are tailored specifically for renovations. They don’t require refinancing your mortgage, have no draw schedules, and leverage your home’s future value which allows you to borrow on average 11x more money for your renovations. This makes RenoFi loans a more convenient and cost-effective choice for homeowners who want to tackle large-scale renovations without the headaches that come with traditional construction loans.

Good Credit Score

A higher credit score makes it easier to qualify for financing. If your score is low, take steps to improve it by paying off debts before applying.

Buying a Fixer-Upper

If you’re eyeing a property that needs major renovations, consider options like the FHA 203(k) or Fannie Mae HomeStyle Renovation loan, which combine the purchase price and renovation costs into one loan. Alternatively, you could secure a conventional first mortgage to purchase the home, then add a RenoFi loan to cover the renovation costs.

Access to Funds

With construction loans, lenders only release funds based on project milestones, which can add complexity to the renovation process. A RenoFi HELOC offers a more straightforward alternative, allowing you to access funds immediately, without the strict requirements around inspections and staged payments that often come with construction loans.

Why Construction Loans Might Not Be Suitable for Renovations

If you’re considering a construction loan for your renovation, it’s good to keep in mind some downsides that might come with this type of financing:

- The draw process can be complex and frustrating for both homeowners and contractors, which may lead to project delays.

- You’ll need multiple inspections throughout the renovation. Scheduling these inspections can add extra steps and delay each payment release.

- There’s often a lot of paperwork involved.

- You may need to refinance your existing mortgage, which could mean losing any favorable interest rates you currently have.

- Closing costs can be higher since they’re based on the total loan amount rather than just renovation expenses. However, this may vary depending on the lender and specific loan terms.

Why RenoFi Might Be a Better Alternative for Remodeling

If you’ve decided that a construction loan isn’t the right fit for your remodeling project, you might want to check out RenoFi Loans for these reasons:

No Need to Refinance

With RenoFi Loans, you can avoid refinancing your existing mortgage because RenoFi Loans are structured as a second mortgage. This allows you to keep your current interest rate on the first mortgage.

No Draws and Inspections

Unlike traditional construction loans, RenoFi Loans make things easier by skipping complex draw schedules and inspections during renovations. Funds are disbursed in full to the homeowner at closing, giving you direct access to the entire amount.

Contractors Love Them

Many contractors prefer working with RenoFi Loans because they simplify the process and cut down on all the paperwork or administrative hassles.

Higher Borrowing Power

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

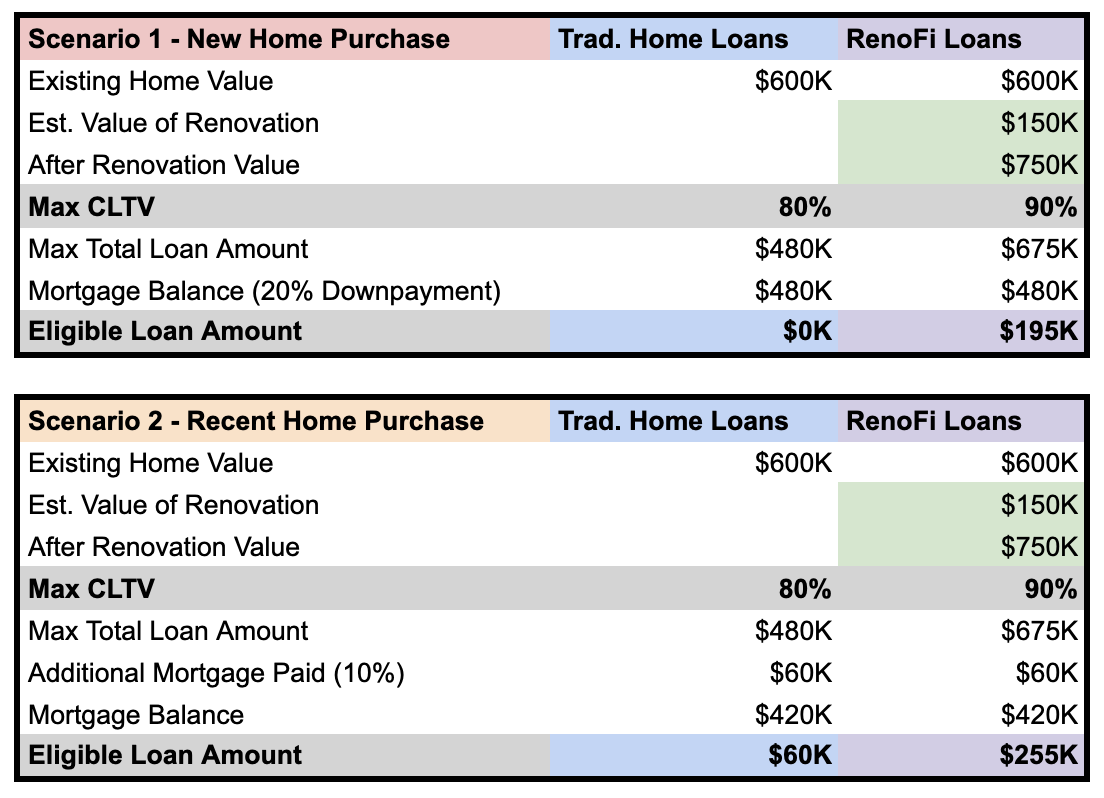

Let’s imagine an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Take Action Today

To wrap up, while a construction loan for remodel can definitely help fund your renovations, there are easier options out there—like RenoFi Loans. They offer more flexibility, so you don’t have to touch your current mortgage rate, plus you can borrow more based on your home’s future value. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.