Construction loans are a type of financing that helps homeowners fund extensive remodeling projects. Since it’s usually used for building new homes, you don’t need to have home equity to qualify.

That said, these loans often come with higher interest rates, especially when compared to options specifically designed for renovations. This is because lenders see construction projects as riskier due to potential delays, cost overruns, and market changes. Plus, these loans are typically short-term.

What Are Construction Loans?

Construction loans are designed specifically for building homes from scratch, but you can also use them for renovating your home.

Unlike traditional mortgages, these loans are short-term and release funds in stages based on project milestones. This way, you can pay your contractors and suppliers as different stages of the project are completed.

One great thing about this approach is that it helps you manage costs effectively as the project moves along. It also means you only pay interest on the amounts you draw, not the total loan amount. This arrangement helps keep your monthly payments lower and more manageable until the project is completed and the loan converts to a permanent mortgage.

The two most common types of construction loans are:

- Construction-to-Permanent Loan: This type combines both construction and permanent financing. It converts into a traditional mortgage once your project is complete.

- Construction-Only Loan: This is just for the construction phase, so you’ll need to get a separate mortgage once the building is complete.

When considering a construction loan for home renovation, keep in mind that closing costs can range from around 2% to 6%, depending on the lender, your location, and other factors. Make sure to factor these into your budget as you consider your options.

Can You Use a Construction Loan for Home Renovation?

Yes, you can use a construction loan for home renovation, even though they are primarily designed for new builds. These loans can help pay for big remodeling projects, especially if you’re making major changes to the structure or layout of your home.

The amount you can borrow often depends on the after renovation value (ARV) of your home, which may allow you to access more funds than you would with other types of loans. This means that if your renovation increases your home’s value significantly, you could borrow more than what your current equity might suggest.

Pros and Cons of Using a Construction Loan for Home Renovation

Pros

- Flexible Funding: Funds are released in stages, allowing you to manage cash flow effectively.

- Higher Borrowing Potential: You may qualify for a larger loan amount based on After Repair Value.

- No Equity Required: You don’t need significant equity in your home to qualify.

- Interest Only on Draws: You only pay interest on the amount disbursed rather than the total loan amount.

Cons

- Potentially Higher Interest Rates: Construction loans usually have higher rates than traditional mortgages, although this can vary depending on the lender, your creditworthiness, and current market conditions.

- Complex Process: The application process can get a bit tricky with all the inspections and draw schedules involved.

- Short-Term Financing: These loans are just for a short time, so you’ll need to refinance into a permanent mortgage once your project is done. That means you could lose any great interest rates you had and might face extra closing costs when you refinance, which can add to the overall expense of the project.

- Potential for Overruns: Renovation projects can run into unexpected issues, such as hidden damage or rising material costs, that might end up costing you more than you originally budgeted.

Alternative Loans for Home Remodel

If a construction loan doesn’t seem like the right fit for your renovation project, here are some renovation-focused alternatives you might want to explore:

- RenoFi Loans: Specifically designed for renovations without refinancing.

- Government Loans: Options like USDA loans, VA loans, and FHA 203(k) loans can help finance renovations.

- Home Equity Loans: These loans allow you to borrow against your existing equity.

- Home Equity Lines of Credit (HELOCs): A revolving line of credit based on your home’s equity.

Why RenoFi Might Be a Better Option for Home Renovation

Contractors Love RenoFi Loans for Their Simplicity

Many contractors prefer working with RenoFi loans because they simplify the financing process. With no draws or inspections required, contractors can focus more on completing your project without getting slowed down by paperwork or administrative delays. This means your renovation gets done faster and with less hassle.

No Need to Refinance

RenoFi loans let you keep your current mortgage rate intact while borrowing against your home’s future value. This means you can get extra cash for renovations without the hassle of refinancing and worrying about losing any great rates you’ve locked in.

Higher Borrowing Power

While traditional options like HELOCs limit borrowing based on current equity (typically up to 90% LTV), RenoFi loans allow you to leverage the after-renovation value (ARV).

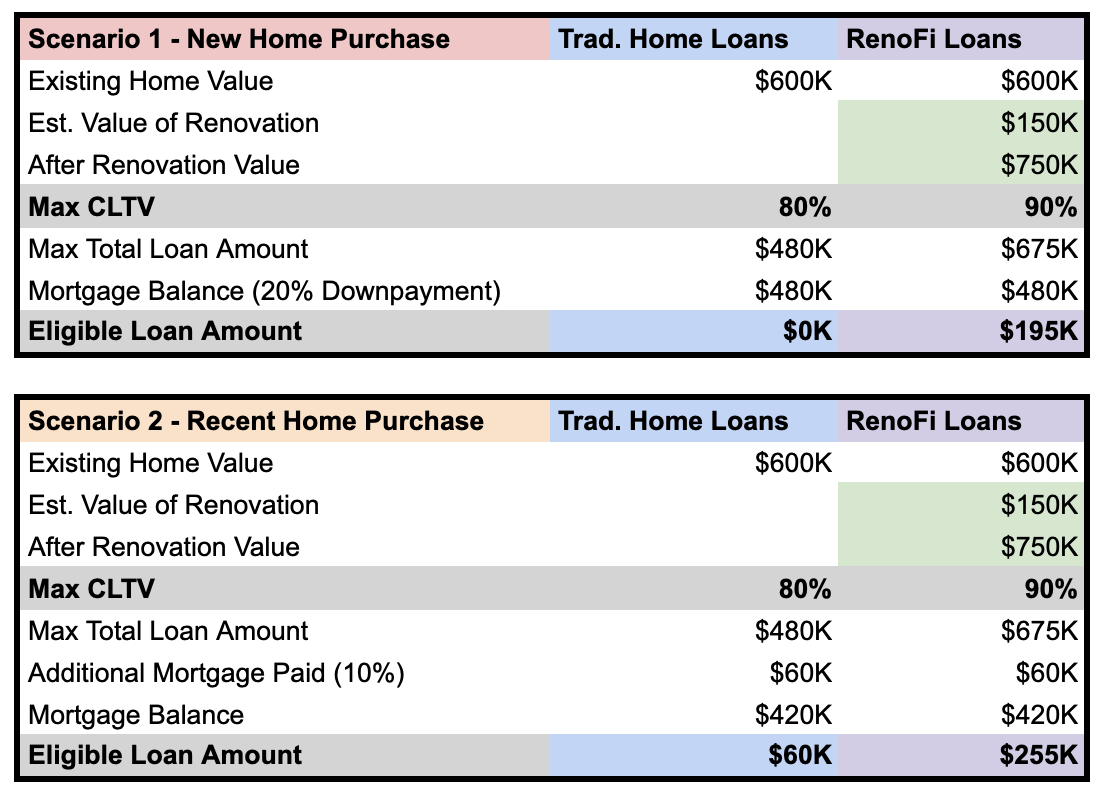

Let’s imagine an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

Using a construction loan for home renovation can be beneficial but comes with its own set of challenges. If you’re looking for a more straightforward solution that maximizes your borrowing potential without refinancing hassles, consider exploring RenoFi options.

RenoFi connects homeowners with credible lenders ready to help finance your renovation project efficiently. Additionally, our RenoFi loans are the smartest way to finance a home renovation project.

Unlike traditional loans, which are based on your current home value or require you to refinance your primary mortgage and give up your low rate, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Contact us today to learn more about how we can assist you.