The best home improvement loans are a great way to finance major renovations, whether you’re looking to upgrade your kitchen, add an extension, build an Accessory Dwelling Unit (ADU), or make energy-efficient upgrades to your home. Opting for the right loan can help ensure your project is funded effectively while keeping costs manageable.

Finding the best financing for your large-scale home improvement projects can be like finding a needle in a haystack. To ease your search, this article will explore various loan options and highlight the pros and cons of each.

1. RenoFi Loans for Major Renovations

Whether you plan on making bigger home improvements like adding a new HVAC system, replacing the roof, or building a backyard deck, or you have more major renovations in mind like remodeling the kitchen or bathroom, replacing old plumbing or electrical systems, or completing modernizing the home, you have several financing options available to you.

For all your major renovation needs, consider the value of RenoFi loans. RenoFi loans allow homeowners to borrow funds based on the property’s after-renovation value, potentially increasing borrowing power compared to traditional loan options.

Best For: Major home renovations, additions, and expenses, such as:

- Full kitchen and bath renovations

- Room additions

- Home expansions

- Basement finishing

- Adding outdoor living spaces

- garage renovations

- Whole house renovations

- Roof replacement

Pros:

- Higher borrowing limits: Loans are based on the after-renovation value of the property

- Flexible financing options: Loans can be structured as home equity loans, lines of credit, or cash-out refinances to fit different needs.

- Potentially lower rates: Interest rates are often more favorable than those of credit card or traditional personal loans.

- Keep your existing mortgage without refinancing: You can potentially keep your existing low interest rate without having to refinance your current mortgage.

- No prepayment penalties: You can pay early with no penalties.

Cons:

- Not for smaller projects: RenoFi loans are best suited for larger renovation projects.

- Possible financial hardship: If the renovation costs exceed the increase in property value, homeowners may end up owing more than the home is worth.

RenoFi loans provide a flexible and accessible financing option for homeowners looking to fund significant renovations based on the home’s future value.

2. Home Equity Loans

A home equity loan allows you to borrow against the equity in your home, making it one of the prevalent options for large-scale renovations. With lower interest rates than unsecured loans, home equity loans are particularly suitable for homeowners who have built up substantial equity in their property.

Best For: Major home renovations or additions, such as:

- Full kitchen remodels

- Room additions or extensions

- Replacing a roof

- Building a garage

Pros:

- Lower interest rates: Since your home secures these loans, they come with lower rates than personal loans

- Fixed monthly payments: Helps with budgeting for large projects

- High loan amounts: Ideal for expensive home improvements

Cons:

- Home as collateral: If you default on the loan, your home is at risk

- Requires significant equity: Homeowners must have substantial equity to qualify

Home equity loans are a reliable choice for large projects that require significant funding. They offer predictable payments and access to large sums of money.

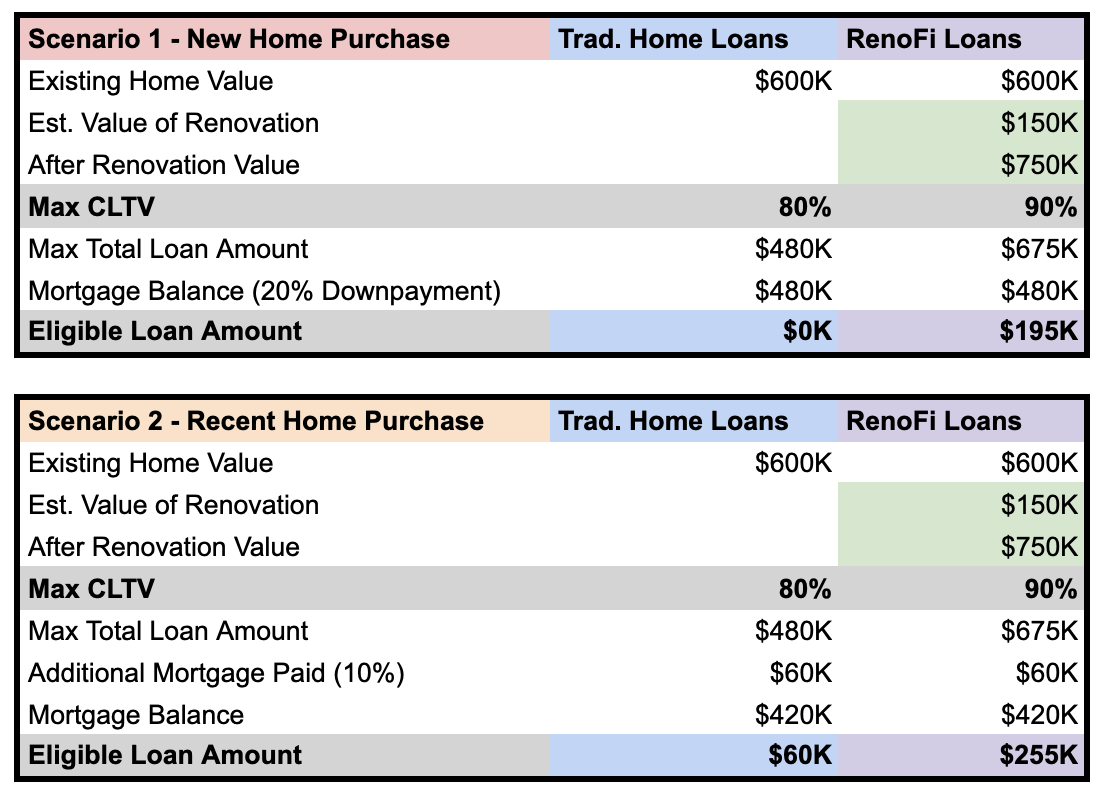

Let’s look at a couple of examples where you want to spend $150,000 to renovate your new home and increase the value of your home.

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Home Equity Line of Credit (HELOC)

HELOCs are another way to access your home’s equity. They function more like a credit card, allowing you to draw money as needed for your renovation. This makes them particularly suitable for long-term or multi-phase projects where costs may spread over time.

Best For: Long-term, multi-phase projects, such as:

- Whole-house renovations

- Adding multiple rooms or an ADU

- Landscaping projects like installing a pool or outdoor kitchen

Pros:

- Flexible borrowing: You only pay interest on the amount you borrow

- Long-term access to funds: Allows for phased projects where costs may vary over time

- Can be used multiple times: A HELOC is ideal if your project requires ongoing funding over the years

Cons:

- Variable interest rates: Leads to unpredictable monthly payments

- Home as collateral: Your home is at risk if you default

- Requires equity: You need to have built significant equity to qualify

HELOCs are good for large, ongoing renovations that may take time to complete, offering the flexibility to access funds whenever you need them.

Now let’s look at how a RenoFi HELOC compares to a traditional HELOC. Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can be 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

4. FHA 203(k) Loans

FHA 203(k) loans are government-insured loans that allow homeowners to finance a home’s purchase and its renovation costs. They’re an excellent option for homeowners looking to make significant structural repairs or those buying a fixer-upper that needs a complete overhaul.

Best For: Fixer-uppers and significant structural repairs, such as:

- Foundation repairs or roof replacement

- Full home renovations or gut remodels

- Projects that require bringing a home up to code

Pros:

- Government-backed: Easier to qualify for, even if you don’t have perfect credit

- Finances both purchase and renovation: Allows you to buy a home and finance renovations with one loan

- Lower down payment: Often lower than traditional loans, making getting started on a big project easier

Cons:

- Lengthy approval process: More paperwork and inspections are required than other loans

- Limited use: Only available for specific types of renovations

FHA 203(k) loans are an excellent option for major renovations that require structural improvements, particularly if you’re purchasing a home that needs significant work.

If you are looking for help with a FHA 203(k) loan, the Renofi Marketplace offers 203k loans through lending partners to help you find lenders for your property.

5. Cash-Out Refinance

A cash-out refinance allows homeowners to replace their existing mortgage with a new one, borrowing more than what is owed and using the difference to fund a large renovation. This is an excellent option for projects that require a substantial amount of money upfront.

Best For: Large-scale, one-time projects, such as:

- Adding a second story

- Building a new wing or significant home addition

- Expensive remodels like a luxury kitchen or bathroom

Pros:

- Lump sum access: Ideal for projects that need substantial funding upfront.

- Lower interest rates: Offers a more affordable alternative than personal loans or credit cards.

- Can reduce your monthly payment: Refinancing can sometimes lower your monthly mortgage payment.

Cons:

- You must qualify for a new mortgage: It can be challenging if your financial situation has changed.

- Increases your mortgage debt: You’ll owe more on your home; failing to make payments could lead to foreclosure.

For homeowners with significant equity, a cash-out refinance is a great way to access large sums for extensive home renovations.

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Which Loan Is Right for You?

- For big projects: A home equity loan or HELOC loan can provide the funding you need with favorable terms.

- For ongoing projects: A HELOC offers flexibility by allowing you to borrow as needed.

- For government-backed options: An FHA 203(k) loan could be the right fit, especially if you’re buying a home that needs major renovations.

If you would like to secure more financing than your home equity, RenoFi is a well-reputed financial institute to consider. They offer loans based on the after-renovation value of your property, which can significantly increase your borrowing power.

Conclusion

Whether planning a kitchen overhaul, a new room addition, or an energy-efficient upgrade, the right home improvement loan can make all the difference. Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.